Factor Investing: Popular but Flawed

Over the last decade we have witnessed the rise (and fall) of many different investment concepts, as investment firms and academics search for a magic formula that can generate consistent returns, whilst crucially avoiding the hard work that is in reality required to generate those returns. Sadly most realize quickly that there is no magic formula for success, so attention instead turns to simply creating sellable investment products. We would argue that sadly today the majority of the finance industry is geared almost entirely towards selling investment products, rather than generating the best long term returns for clients.

One of the most popular of these recent concepts is ‘Factor Investing’, which has proved to be a highly sellable investment strategy over the last decade; gathering billions of dollars in assets. This has been an easy product for many firms to market and sell as it comes backed by reputable academics and with impressive mathematical support. However, in the real world this concept faces significant shortcomings that raise serious questions about its validity when it comes to being able to generate consistent long term returns.

Please note that when we say ‘Factor Investing’ here we aren’t referring to the notion that arguably all investing involves looking at ‘factors’ or variables; both qualitative and quantitative, but we are instead referring to the specific practice of using statistical methods to mine the most (seemingly) predictive factors of the past and then use them algorithmically to make investment decisions going forward. The meteoric rise of this kind of ‘Factor Investing’ has been in large part driven by Wall Street which, seeing an opportunity to earn generous fees with relatively little work, has been heavily involved in promoting and selling the concept.

It might surprise you to learn that Factor Investing as a strategy is nothing new nor technologically advanced. The idea was pioneered roughly fifty years ago in a 1976 paper by Stephen Ross, who argued that security returns were best explained by multiple ‘factors’ which could be fed into an algorithm to predict returns. For many years the idea did not gain much traction – possibly because most investors at that time still believed a stock was actually a share in a real business, rather than just the output of some statistical model (the good old days).

But that sensible approach to investing sadly would not last. In the 1990s, Factor Investing finally got its marketing message right – in large part due to the work of Eugene Fama and Kenneth French (two career academics, not investors) who took the idea and developed it into a sellable product that the finance industry could really run with. The academics did such a good job of repackaging and presenting the idea that today hundreds of billions of dollars of assets are now invested in purely factor-based strategies.

What is Factor Investing?

Factor Investing involves identifying characteristics or ‘factors’ that can be used to explain stock returns. There are many, many factors that academics have identified over the years that can be used (in hindsight) to explain stock returns. The most common of which are:

- Company size

- Growth

- Valuation

- Profitability

- Leverage

- Momentum

The three factors that Fama and French used when they popularized the idea back in the 1990s were company size, past performance, and valuation based on book value. For those of you mathematically inclined, their formula for predicting stock returns was as follows:

Rit − Rft = αit + β1(RMt − Rft) + β2SMBt + β3HMLt + ϵit

Where:

Rit = total return of a stock or portfolio i at time t

Rft = risk free rate of return at time t

RMt = total market portfolio returns at time t

Rit−Rft = expected excess return

RMt−Rft = excess return on the market portfolio (index)

SMBt = size premium (small minus big)

HMLt = value premium (high minus low)

β1,2,3 = factor coefficients

Let us walk through this step by step. In plain English: The return of a stock (over and above a risk free return such as cash or treasuries) will be determined by the amount the stock has recently outperformed the market (positively correlated), the size of the company (negatively correlated, small cap premium), and finally the valuation level of the company, defined as book to market value (positively correlated, value premium).

Now, let us think through the logic behind those three factors as ‘predictors’ of future stock returns.

We can give them some credit for identifying that valuation, i.e. that the price you pay for an investment, is going to impact your return. However, we cannot give them too much credit for their choice of book value as a single valuation metric, which is flawed to the point of being useless. For example, Facebook has relatively few hard assets and therefore very little book value but has been one of the best performing businesses of the past decade. Would we have been better off buying a coal power plant instead of Facebook just because it had more hard assets on its balance sheet? Clearly not.

When it comes to the other two factors; the size of a company and its past performance, both are obviously not relevant factors in determining future success. The performance of Apple in the next 5 years will be determined by how many iPhones they sell, and how profitable their new products and services are. It will not be determined by either the size of Apple as a company, nor by how profitable their past products and services were. Said another way, the performance of a stock in the past tells us nothing about what that stock is going to do in the future. It does not consider industry shifts, competition changes, new regulation, global pandemics, etc. Whatever the stock price has done beforehand is an irrelevance. Similarly, deciding that one company will outperform another in the future simply because it is smaller, is clearly a flawed way to select businesses in which to invest.

However, we should not spend too much time criticizing the original Fama and French three-factor model. Factor Investing true believers would argue that they have gotten much better at picking and tweaking factors – creating models that are much more robust today than in the past. So instead, let us take a step back and focus on the fundamental argument that is the foundation for all Factor Investing: which is that the future performance of a stock (on average) can be determined by a set of quantifiable, backward-looking variables.

There are three main issues with this statement:

- Factor Investing relies on what is quantifiable.

- Factor Investing relies on historical data.

- Factor Investing relies on factor discovery not reducing factor returns.

Let us take these one by one:

First, Factor Investing relies on what is quantifiable

As the quote we opened this piece with states, not everything that can be counted counts and not everything that counts can be counted.

Imagine that we want to predict which car will win a race, so we compile data on every motor race that has ever happened since 1910 in order to see which factors have the most statistically significant predictive power. We might find that some factors such as engine type, driver age, etc, have some predictive power. We might also find that 90% of race winning cars happened to be painted red which (even if it logically does not make sense) would imply very high predictive power. We trust our math, so we add it to our model.

But what about all the factors that go into a race that are not easily quantifiable. Like how good is the driver? How do we measure how good they are? Do we have to arbitrarily ascribe a number to this qualitative attribute? Are they a “25” good? What would that even mean? How good is the team? What about the unpredictable weather, or the odds of another driver crashing into our driver at no fault of their own? We intuitively know that all of this matters more than the color of the car, but since it does not easily fit into our statistical model, a factor approach will leave it out and instead pick winners based on the color of the car.

How does our car example relate to real life Factor Investing? With most statistical modeling, the predictive power of a variable is based on its R2 (the coefficient of determination), calculated by running historic regressions of the performance of two variables, i.e. stock performance and the factor itself. As you can imagine, this is a data and math heavy process that does not lend itself to qualitative factors that are not easily represented by a hard number.

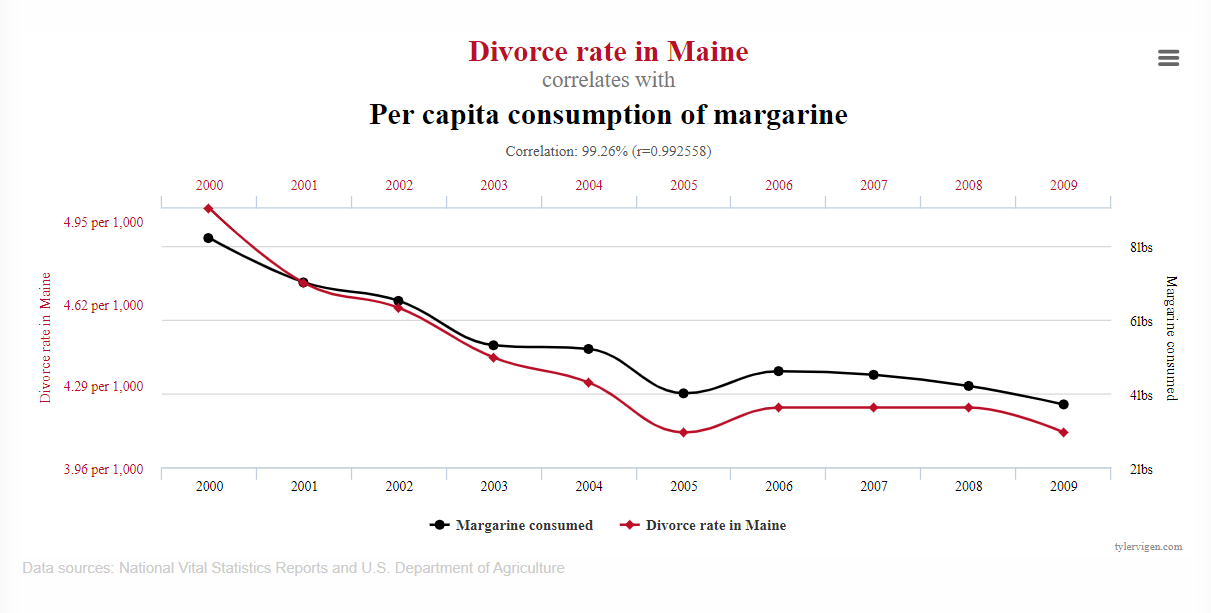

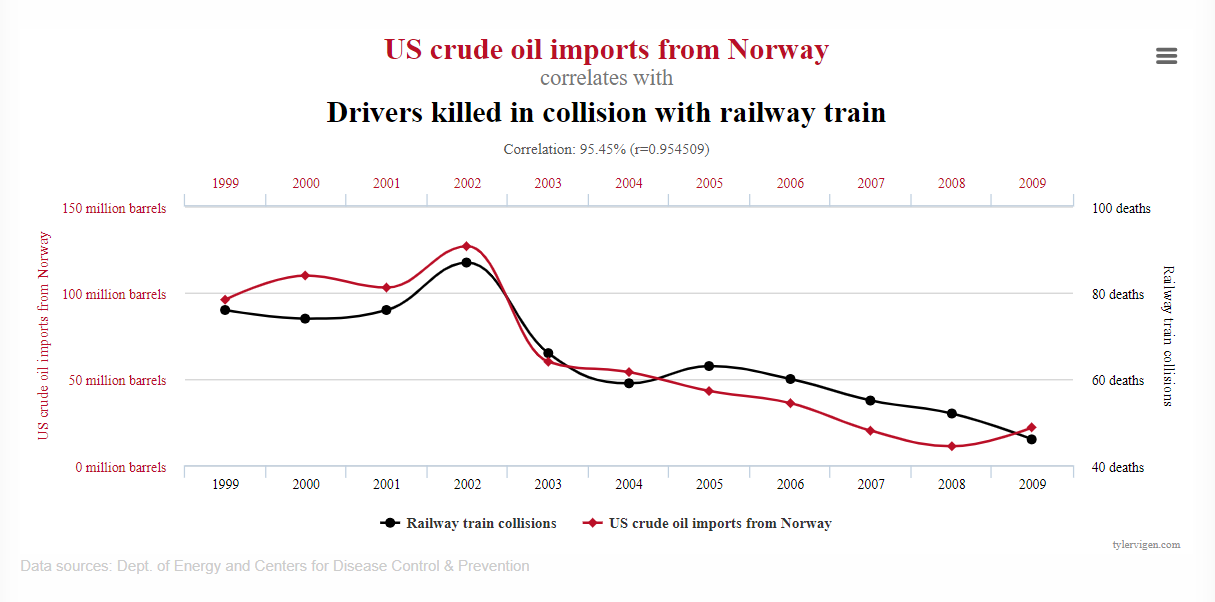

When Fama and French popularized the idea, they identified that the R2 of their three factors were all around 90%, which statistically implies a strong relationship between variables. But as our red car example illustrates, strong correlation does not equal strong causation. There exist within the world around us thousands of correlations with high statistical predictive power that make no logical sense whatsoever. For example:

Clearly these are nonsense and those factors cannot be used to predict one another; but in both examples the statistical predictive power is actually stronger than that of the factors identified in the Fama and French model. Once again, just because something can be counted does not mean it counts.

Now, you might accuse us of being overly hyperbolic, but academics and senior investment professionals have genuinely argued that their factor based correlation data is so compelling that it doesn’t matter if they simply ignore all of the underlying qualitative factors of a business: who is running it, how good the product or service is, what are the competitive threats, how the employees and management team are incentivized etc. and instead base their investing decisions purely on the factors that are most statistically powerful.

Consider this recent Bloomberg interview with a senior executive at Blackrock, one of the world’s largest money managers, that takes this idea even further. They argue that valuing a business based on any fundamental factor is a futile exercise, so instead one should scour vast amounts of alternative data (i.e. the color of the car) to find more powerful correlations on which to base investment decisions:

“money managers need new investing methods because there’s no way to tell if betting on ostensibly cheap companies will work again. In fact, comparing share prices to fundamentals like corporate profits or book value is essentially futile in complex markets.”

Has the investment industry completely lost track of what investing is? Has everyone forgotten that stocks represent an ownership share in a real business? If you are going to buy an ownership share in any business, surely you need to at least attempt to value that business? The fact that so many in our industry think otherwise is quite frankly alarming.

We think this comes back to the path of least resistance and what is most easily sellable. Factor Investing, with quantitative factors that can easily be plugged into a model and put on a set it and forget it strategy, is both easy and sellable. Actually doing the hard, qualitative work of figuring out which businesses are best positioned to win in their respective marketplaces over the long run is difficult, but this is also why algorithmic Factor Investing will always be at a disadvantage to humans who can think critically and qualitatively.

Second, Factor Investing relies on historical data to predict the future

Sticking with our race car example, we might discover that a certain type of car or engine has won 90% of races in the past. Again, we say great, and plug that factor into our model and start making predictions. But what if there is a new engine technology that has just been released on the racing scene that drastically outperforms the engines of the past? Just like that our model based on the past stops working.

This happens all the time in business – markets change, interest rates move, new products emerge, regulations shift, consumer preferences adapt. Think of Blockbuster, Kodak, Nokia, etc. In each case, investors could have avoided significant losses if they focused on the underlying business and how the industry and competition were evolving rather than focusing on what backwards looking data would predict.

The reason these backward-looking factors are not useful comes back to a fundamental truth: the entire set of past outcomes does not include the entire set of all possible future outcomes. Said another way, just because a given stock or market has only fallen or risen by X% in the past, does not mean that it cannot fall or rise by more than X% in the future. Trusting historic averages is not only inadvisable, it is downright dangerous.

If you need any proof of this, just look back to the crisis of 2008 which was caused, in most part, by backwards looking risk models that assumed that just because house prices had never fallen significantly at the same time across the nation in the past, that they would never do so in the future. That turned out to be a devastatingly wrong assumption based entirely on backwards looking data.

Third, Factor Investing relies on factor discovery not reducing factor returns going forward

Think about this logically – if we were to come up with a magic factor-based formula that automatically prints money in the stock market then surely we wouldn’t want that formula to get out and reach mass adoption, right?

Because in doing so this would only serve to reduce the money printing power of that formula. This is because the factors used would get bid up by other investors using the same formula until there was no more profit to be had. For example, if investors discover low P/E ratio stocks correlate with higher returns, then others buy into that idea and bid up low P/E stocks, until the P/E factor-based model ultimately stops working.

So, why then is it that Wall Street is so eager to market these money printing formulas and give up all the riches they could amass by keeping them secret for themselves? If you think it is due to altruism, we have a bridge to sell you.

The real reason is that the success (or failure) of Factor Investing does not actually matter to those who create and sell Factor based products. What matters to them is just that Factor Investing is a sellable product/ strategy. And boy has it become sellable in the last two decades now that it comes with the stamp of approval from noble prize-winning academics and an impressive complicated algorithm backing it up. Remember that it took fifty years for Factor Investing to catch on? The concept remains as flawed today as it was then, the only difference now is that the marketing message has gotten a lot better.

This is a sad reflection of the investment industry in general – being successful often does not require actual investment skill nor a great track record. Being successful is often just defined by creating sellable products and strategies, and the more jargon or incomprehensible math you can put behind those products, the easier it is to sell them. Regardless of how questionable the logic is on which they are built.

For the big firms, all the products must do is perform well enough to not attract attention. And even if a product or strategy does attract attention for performing poorly, they can easily pick one of a hundred other newly created products or factors to invest you in instead. The only people getting rich here are the companies who create these products and sell these strategies – not the end investors whose money is getting shuffled around from spurious strategy to spurious strategy.

Conclusion

We need to always remember two important facts – stocks represent ownership in a business, and the returns of any stock over the long run will always track the underlying performance of the business itself. Reread that a hundred times. Stick it on your bathroom mirror.

The market may undervalue or overvalue companies in the short term, but if a company grinds out consistent earnings and cashflow growth year after year and invests its capital wisely, then that will eventually be reflected in the share price.

Conversely, if a company produces no cash at all and runs at a loss, it can only get away with that for so long. Few businesses can survive a decade without any positive cash flow, no matter what your momentum factor strategy might suggest. Investors will only fund a loss-making operation for so long.

This is the real causal relationship that drives stock returns. Not the various statistically significant factors that have historically correlated with stock returns. Remember: do not confuse correlation with causation, cars do not win races just because they are painted red.

Disclosures: This website is for informational purposes only and does not constitute an offer to provide advisory or other services by Globescan in any jurisdiction in which such offer would be unlawful under the securities laws of such jurisdiction. The information contained on this website should not be construed as financial or investment advice on any subject matter and statements contained herein are the opinions of Globescan and are not to be construed as guarantees, warranties or predictions of future events, portfolio allocations, portfolio results, investment returns, or other outcomes. Viewers of this website should not assume that all recommendations will be profitable, or that future investment and/or portfolio performance will be profitable or favorable. Globescan expressly disclaims all liability in respect to actions taken based on any or all of the information on this website.

There are links to third-party websites on the internet contained in this website. We provide these links because we believe these websites contain information that might be useful, interesting and or helpful to your professional activities. Globescan has no affiliation or agreement with any linked website. The fact that we provide links to these websites does not mean that we endorse the owner or operator of the respective website or any products or services offered through these sites. We cannot and do not review or endorse or approve the information in these websites, nor does Globescan warrant that a linked site will be free of computer viruses or other harmful code that can impact your computer or other web-access device. The linked sites are not under the control of Globescan, and we are not responsible for the contents of any linked site or any link contained in a linked site. By using this web site to search for or link to another site, you agree and understand that such use is at your own risk.