Third Quarter 2023 Update

Dear Partners,

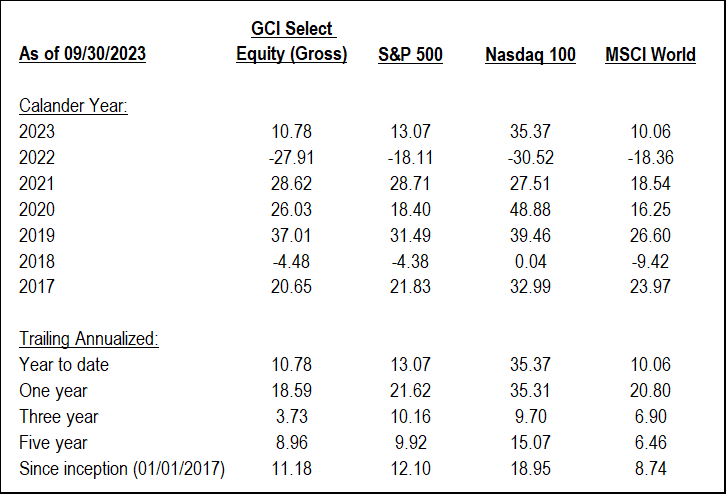

The third quarter of 2023 saw a return of volatility in equity markets as the 10-year treasury yield spiked to levels not seen in more than 15 years. Against this backdrop, our GCI Select Equity strategy gave back some performance, however, our year-to-date numbers continue to be strong on an absolute basis while lagging slightly on a relative basis.

As you will recall, we began this year with a banking crisis, followed by a significant rally in technology names as the AI narrative took hold, followed by a steep pullback during the month of September. As long-time partners will know, we do not see the recent spike in share price volatility as anything to be concerned about. Rather, we see volatility as the friend of the long-term, fundamentals-based investor – providing us with the opportunity to add new or to increase our holdings in names where the share price and underlying business value may be diverging.

GCI was founded on the principle that investing in high-quality companies at attractive prices is the most durable and consistent way to achieve long-run, risk-adjusted returns. As such, we will continue to avoid short-term market timing efforts, nor will we chase the overvalued names that are currently holding up the market indices (Nvidia, Tesla, Apple, etc.). Instead, we will continue to do what we have always done – to partner with truly exceptional businesses where we can be confident that our shareholder value will compound over time.

Portfolio Update

Year-to-date, our three best-performing positions are Booking Holdings (BKNG), Amazon (AMZN), and Alphabet (GOOGL) – each of which is up nearly 50%. Our three worst-performing positions are Crown Castle (CCI), Charles Schwab (SCHW), and American Tower (AMT) – each of which is down nearly 30%.

As usual, we will spend little time on what is currently working and instead spend this letter talking more about what hasn’t worked this year. We have already talked at length about Charles Schwab in past letters so we will spend most of this letter talking about Crown Castle and American Tower, two cellular tower REITs that sold off heavily in the month of September.

Recall that cellular towers are very valuable assets, as they are the bottleneck when it comes to us all consuming more and more mobile data. These companies simply own physical towers and then rent space on them to the carrier companies (AT&T, Verizon, T-Mobile, etc.) to affix their equipment on. Service contracts are typically 10-20 years in duration with fixed escalators of roughly 3% (international contracts tend to be inflation-linked) – which results in a predictably cash-generative business.

Both companies lay squarely in the middle of a huge, multi-decade secular trend – the exponential growth of mobile data consumption driven by ever-increasing smartphone penetration, faster available mobile internet speeds, huge growth in video content being consumed on mobile devices, as well the growth in the number of internet-enabled devices. It is almost a certainty that year over year – regardless of politics, wars, or any external influence – we will continue to consume more mobile data.

The attractive returns here are protected due to it being very hard to build any new towers as zoning is difficult to achieve – no one wants a big metal tower in their backyard. American Tower reinvests cash from this cash-cow of a business into buying new towers in faster-growing and much earlier-stage markets like Brazil and India.

Crown Castle takes a different approach, reinvesting cash into building out a “small-cell” network in the United States – think of these like mini towers that are placed on lamp posts, traffic lights, etc. in dense urban areas where macro towers can’t be placed – the competitive moat being the fiber backbone that is required to make these small-cells function (CCI have invested over $14bn in buying fiber networks, making them one of the largest fiber owners in the US).

Year-to-date, both these companies have gotten caught up in a broad-based selloff of REIT companies due in large part to the rising interest rate environment (rates go up, valuations go down). For us, short-term valuation volatility is of little concern. What does concern us is when our businesses face the possibility of deteriorating fundamental economics over the long run. Based on the structural advantages these businesses have, we see long-term impairment as an unlikely outcome.

One longer-term risk that is often cited by bears is that maybe in 20 to 30 years satellites will improve enough to be comparable to cellular towers (think Starlink). Firstly, satellites are much more expensive than towers (which are often just a few steel beams stacked upright) due to the fact that they need to be launched into orbit and then relaunched about every 10 years due to decay.

Secondly, even if launching and maintaining satellites did somehow become cost-competitive with cellular towers, there is then still the law of physics to contend with – latency will always be affected by the sheer distance signals must travel and throughput will always depend on frequency and loss rates (more distance traveled, more things that get in the way).

Lastly, even if cost and physics were both somehow overcome, there is still the issue that all the carrier companies have 10-20-year contracts with the towers and can’t run both tower signals and satellite signals at the same time to the same location due to interference. So, a carrier would need to wait for their contract to end, and then shift all their service over to satellites, and then hope nothing goes wrong with the service. As such, we don’t give much credence to the satellite threat – instead, satellites will continue to serve markets that Towers can’t like flights, ocean vessels, and rural markets that haven’t yet been connected to with fiber lines.

Today, American Tower trades for roughly a 6% NTM AFFO yield and Crown Castle trades for roughly an 8% NTM AFFO yield. Worst case, both companies should grow earnings by at least 3% over the next decade due to their built-in contract escalators. This would imply a total shareholder return of no less than 9-11% going forward which should be much higher than that when we consider their growth investments. For us, we never underwrote these investments assuming interest rates would stay at zero forever, so we have seen the recent sell-off as increasing our expected returns going forward. As such, we have been adding to our positions.

As always, please feel free to reach out to us if you have any questions or would like to schedule a one-on-one meeting with us to discuss further.

Kind regards,

Guy Davis, CFA

David Shahrestani, CFA

Disclosures: This website is for informational purposes only and does not constitute an offer to provide advisory or other services by GCI Investors in any jurisdiction in which such offer would be unlawful under the securities laws of such jurisdiction. The information contained on this website should not be construed as financial or investment advice on any subject matter and statements contained herein are the opinions of GCI Investors and are not to be construed as guarantees, warranties or predictions of future events, portfolio allocations, portfolio results, investment returns, or other outcomes. Viewers of this website should not assume that all recommendations will be profitable, or that future investment and/or portfolio performance will be profitable or favorable. GCI Investors expressly disclaims all liability in respect to actions taken based on any or all of the information on this website.

There are links to third-party websites on the internet contained in this website. We provide these links because we believe these websites contain information that might be useful, interesting and or helpful to your professional activities. GCI Investors has no affiliation or agreement with any linked website. The fact that we provide links to these websites does not mean that we endorse the owner or operator of the respective website or any products or services offered through these sites. We cannot and do not review or endorse or approve the information in these websites, nor does GCI Investors warrant that a linked site will be free of computer viruses or other harmful code that can impact your computer or other web-access device. The linked sites are not under the control of GCI Investors, and we are not responsible for the contents of any linked site or any link contained in a linked site. By using this web site to search for or link to another site, you agree and understand that such use is at your own risk.

All references and views offered, including but not limited to stocks, companies, investments, investment styles, market returns, expectations, forecasts or estimates and any other area of investing are the opinion of the manager and should not be taken as facts, projections or guarantees. All such opinions are subject to change are do not constitute a recommendation or solicitation to buy or sell a particular security.