First Quarter 2023 Update

Dear Partners,

Markets continued to experience significant volatility in the first quarter of 2023. Inflation worries, recession risks, and the first bank failure in over 15 years all contributed to more underlying equity weakness than apparent in the headline numbers. Indices were largely held up in the quarter by significant outperformance in Mega-cap Technology – namely Apple and Microsoft which now make up roughly 14% of the S&P 500 index and roughly 25% of the NASDAQ 100 index. A stark reminder that passive investing isn’t as diversified nor as low risk as it is often marketed as.

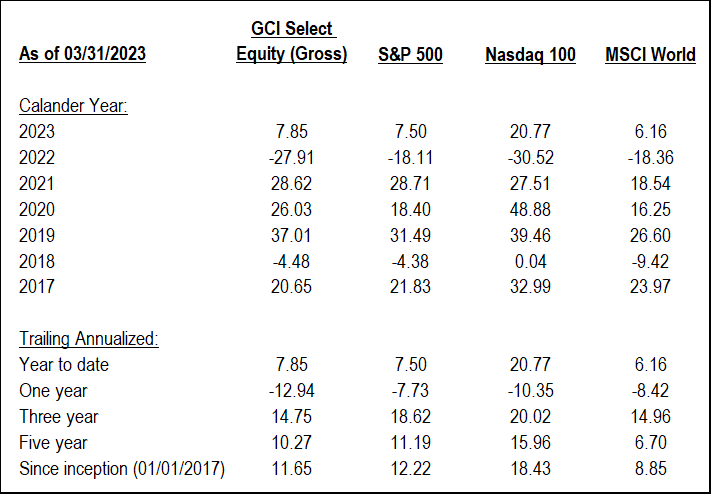

Against this backdrop, our GCI Select Equity strategy produced solid absolute returns and modest relative performance.

This performance was achieved despite us running a concentrated portfolio that included Charles Schwab (SCHW) which was unfortunately down nearly 40% in the quarter as Schwab was swept up in the panic surrounding SVB and the regional banks. As we already noted in our recent update, we feel that this was a short-term over reaction by the market and we used the opportunity to add to our position.

The failure of SVB is without doubt a significant event for the economy and we will continue to monitor this situation closely. Bank failures are rare, and if not managed correctly can quickly have knock-on effects. In this situation, we believe that the regulators did the right thing (and the only thing they could do) by guaranteeing all deposits at SVB almost immediately. Without that step, the deposit flight that we’ve seen at regional banks elsewhere would’ve likely been far worse.

Regarding Charles Schwab specifically, the reasons for our confidence and addition to the position can be found at the link above. But to summarize – the market is currently worried that if Schwab was forced (due to a run on their deposits) to sell their Held-to-Maturity securities and take losses, then they would also need to raise dilutive capital to stay in the regulator’s good graces, leading to a vicious cycle of share price pressure. This is the situation that led to SVB’s downfall.

Firstly, brokerages are different from banks. A run on a brokerage is extremely unlikely given the ring fencing of client assets. In fact, brokerages have been reporting asset inflows during this period as bank depositors seek higher yielding refuge in the securities markets. However, Schwab does face issues with cash sorting, as Schwab bank deposits, which Schwab earns a spread on, are moved to higher yielding securities. How worried should we be about this cash sorting?

In a recent Wall Street Journal interview Walt Bettinger (Schwab CEO) talked about what would occur even if a total deposit flight did take hold: “There would be a sufficient amount of liquidity right there to cover if 100% of our bank’s deposits ran off. Without having to sell a single security.” Now, we are always conscious of taking any CEO’s comments with a pinch of salt, but not only do we agree with that assessment, but management at Schwab have also gone one step further by putting their money where their mouth is and purchasing roughly $7.5M of Schwab stock in their personal accounts since the panic began on March 14th – a welcome show of confidence.

None of this is to say that Schwab won’t have short-term earnings pressure as their low-cost deposits are replaced with higher cost funding sources. But as we have always said before, the market’s narrow focus on short-term issues is what creates opportunities for us as long-term investors.

Looking at the long-run, Schwab has built a strong foundation to continue taking market share and organically grow their total client asset base for many decades to come. Pair that with the transactional need for clients to always have some money sitting in cash at Schwab bank, along with the current higher interest rate levels that Schwab can put these new assets to work at, and we believe Schwab’s future earnings power will be much higher than today’s.

As always, we would like to take this opportunity to thank you, our partners, for your continued trust in us and our approach. After all, the success of any investment strategy depends on a mutual understanding between us as the manager, and you as our investors and partners on what our ultimate goal is and how we intend to achieve it.

For us at GCI, that has always meant investing in high-quality companies at attractive prices.

Please feel free to reach out to us with any questions you may have, or if you would like to discuss any of this further.

Kind Regards,

Guy Davis, CFA

David Shahrestani, CFA

Disclosures: This website is for informational purposes only and does not constitute an offer to provide advisory or other services by GCI Investors in any jurisdiction in which such offer would be unlawful under the securities laws of such jurisdiction. The information contained on this website should not be construed as financial or investment advice on any subject matter and statements contained herein are the opinions of GCI Investors and are not to be construed as guarantees, warranties or predictions of future events, portfolio allocations, portfolio results, investment returns, or other outcomes. Viewers of this website should not assume that all recommendations will be profitable, or that future investment and/or portfolio performance will be profitable or favorable. GCI Investors expressly disclaims all liability in respect to actions taken based on any or all of the information on this website.

There are links to third-party websites on the internet contained in this website. We provide these links because we believe these websites contain information that might be useful, interesting and or helpful to your professional activities. GCI Investors has no affiliation or agreement with any linked website. The fact that we provide links to these websites does not mean that we endorse the owner or operator of the respective website or any products or services offered through these sites. We cannot and do not review or endorse or approve the information in these websites, nor does GCI Investors warrant that a linked site will be free of computer viruses or other harmful code that can impact your computer or other web-access device. The linked sites are not under the control of GCI Investors, and we are not responsible for the contents of any linked site or any link contained in a linked site. By using this web site to search for or link to another site, you agree and understand that such use is at your own risk.

All references and views offered, including but not limited to stocks, companies, investments, investment styles, market returns, expectations, forecasts or estimates and any other area of investing are the opinion of the manager and should not be taken as facts, projections or guarantees. All such opinions are subject to change are do not constitute a recommendation or solicitation to buy or sell a particular security.