Second Quarter 2023 Update

Dear Partners,

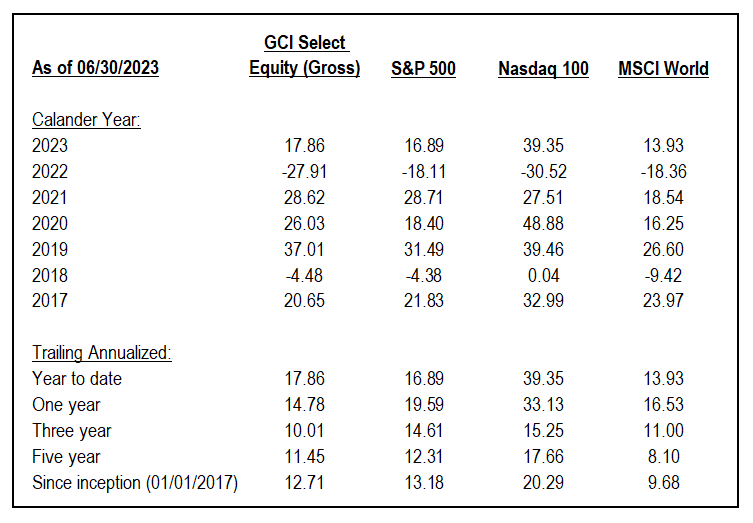

After significant volatility to begin the year, the second quarter of 2023 saw a much steadier move higher in equity markets. Against this backdrop, our GCI Select Equity strategy produced solid absolute returns and modest relative performance.

The move higher in equity markets this quarter was almost entirely due to outperformance in Mega-cap Technology names. Recall that in our last update we highlighted how Apple and Microsoft together now make up north of 14% of the S&P 500 index and north of 25% of the NASDAQ 100 index. Both names are up more than 40% this year, lifting the indexes up along with them.

Now, we would be remiss if we did not spend at least some time in this update talking about the recent narrative surrounding AI and more specifically the performance of Nvidia (a company we don’t own) over the first half of this year – up nearly 200%, growing to a market cap of $1T.

With regards to AI, you will likely have read about or tried out the new ChatGPT product from OpenAI. The importance of ChatGPT’s launch was not so much in the technology itself (Large Language Models have been around for a while albeit not publicly) but in how it was packaged in a way that made the technology actionable and relatable to almost everyone – artists, students, business executives, etc. ChatGPT was the first product that gave us a glimpse of the utility we might gain as a society as this technology is refined and perfected.

However, as has been true with each paradigm-shifting technology that came before – the personal computer, the internet, smartphones, social media, etc. – markets tend to get ahead of themselves in bidding up every possible winner, despite history showing time and again that early winners in these revolutions (Macintosh PC, Yahoo, Blackberry, MySpace, etc.) are rarely the same winners a decade later (Windows PC, Google, iPhone, Facebook, etc.) not to mention the disruption to older industries that are displaced by these new technologies entirely.

The most important thing to remember regarding these “revolutionary technology” narratives we hear about in the media is that you can accurately predict that a technology will be revolutionary and still lose a lot of money betting on it as an investor – just look to the history of the automotive or airline industries. The better strategy is to continue looking at businesses on a case-by-case basis, focusing investment dollars solely where there is high confidence in what earnings power will be a decade from now regardless of whatever happens with this AI revolution.

Which brings us to Nvidia, a specific company that the market is currently betting will win the AI revolution. How likely is this? And more importantly, even if they do win, will investors win as well at today’s valuations?

The history here is interesting and it is worth setting up the context to answer these questions. Over the past four decades, we went from CPUs (core processing units) processing single commands (threads) at a time, to multi-core CPUs processing parallel threads.

But for use cases geared solely to parallel processing – those with operations that are independent of each other – GPUs (graphic processing units) eventually proved much more efficient. Whereas CPUs were optimized for speed, GPUs were optimized for throughput.

So, in the early days, the main use case for GPUs was rendering 3D graphics in gaming programs, which required millions of little polygons stitched together based on coordinates and some matrix math (move, shrink, enlarge, rotate, etc.) Hence Nvidia was born and spent much of its history as a gaming graphics company selling GPUs.

But then flash forward a couple of decades later and a new, faster-growing, and even larger market for GPUs opened. It turned out that many modern machine learning techniques (neural networks, reinforcement learning, large language models such as ChatGPT, etc.) are built around the same matrix math that rendering 3D graphics is. This put Nvidia in a great position to pivot to this fast-growing market.

This early lead would normally be competed away by other companies like Intel, AMD, etc. but the secret sauce for Nvidia was their proprietary software, CUDA. To simplify this a little, for hardware and software to talk to each other, often the software must be specifically designed for the hardware. CUDA simplified this process so that any AI researcher could develop programs on top of CUDA, and they would know those programs would always work so long as they were using Nvidia’s GPUs.

As developers coalesced around the ease of CUDA (helped a lot by Nvidia’s already established installed base), they created the tools to support the ecosystem, which then incentivized other developers to join and do the same. Even if the large cloud infrastructure providers wanted to move their own internal workloads to proprietary chipsets, they would still be required to purchase Nvidia’s GPUs for their customers’ use cases, so long as that was what their customers demanded.

This is what created Nvidia’s moat and along with the secular trend of AI penetration has been responsible for the massive share price appreciation we have seen in the stock over the past decade, as well as this year.

And going forward, Nvidia is likely going to continue to benefit from these trends – providing the foundational technology to just about every major technology trend (autonomous driving, edge computing, IoT, VR, AR, machine learning, big data, etc.). The problem, however, is valuation. Nvidia is now trading at nearly 40x (albeit depressed) sales, levels rarely seen for smaller startups, much less so for $1T companies.

To justify today’s valuation, we would need to believe Nvidia will be able to more than 20x their revenue over the next decade while more than doubling their margins. While this could technically be possible, in real dollar terms it is extremely unlikely. In other words, an investment in Nvidia at today’s valuation has very little margin of safety, everything needs to go perfectly just to receive a modest return.

The main takeaway here for us as investors is that valuation always matters – no matter how high quality a business may seem, nor how exciting the narrative around it may be, you can always lose money by buying a great company at the wrong price. This is especially true around hyped-up narratives like we are seeing with AI.

Portfolio Update

We usually spend this time talking about our investment losers, as the winners tend to take care of themselves. This year we have already spent a considerable amount of time talking about our biggest loser, Charles Schwab Corporation, and why we believe it is being unfairly punished by the markets. Our other biggest losers this year are Crown Castle and American Tower, two cellular tower REITs.

There is nothing particularly interesting to say about the performance of these two companies; there have been no bank runs, as was the case with Charles Schwab, rather the valuation the market puts on these two companies has simply compressed alongside rising rates.

The cell tower companies in general continue to represent one of the most secure and stable future revenue streams that we have around us – there simply is no scenario where mobile data consumption does not increase each and year, and the towers are the ‘pipes’ through which all this data is delivered. As long-term investors, the security of long-term cash flows from these assets remains very attractive.

With the yield on the 10-year treasury currently hovering below 4%, we are very comfortable continuing to own these tower companies (which are some of the best businesses in the world) at roughly 5% dividend yields – which, unlike bonds, should continue growing their distributions at HSD rates for many years to come.

On a more positive note, we thought it would be helpful to highlight two of our best performers this year: Copart (a relatively recent addition) and GFL (our largest single-stock position). Despite these companies having zero exposure to the AI narrative, in fact, being remarkably ‘analog’, they have both performed very well for us – Copart is up ~50% YTD and GFL Environmental ~30% YTD.

Both companies operate in simple but critically important industries. For Copart, they operate in the auto salvage market – ensuring that when vehicles are totaled in collisions there is the physical infrastructure in place to both store and sell those vehicles. GFL operates in the waste management industry – similarly ensuring that our day-to-day waste is picked up and disposed of.

While both companies have unique drivers that are attributable to their investment success this year, the main point we want to get across is that one does not need to participate in the AI hype (or indeed any of the ‘next greatest thing’ hypes) to have great success as an investor. Both Copart and GFL provide essential services for society that are still going to be required decades from now, no matter what happens or doesn’t happen with AI. And best of all, we get to own these businesses at attractive valuations.

As Warren Buffett has said before, we would rather be confident of a good outcome than simply hopeful of a great one. As you know, GCI Investors was founded on the principle that investing in high-quality companies at attractive prices is the most durable and consistent way to achieve long-run, risk-adjusted returns. We will continue to do just that.

TD Ameritrade & Charles Schwab Integration Update

As a brief reminder, TD Ameritrade (our custodial brokerage) and Schwab continue to make progress on the integration of their two firms with the final transition date set for September 5, 2023. By now, you will have begun to receive communication from TD about the change.

The key thing for you to be aware of is that there is nothing for you to do in order to maintain your portfolio holdings – Schwab will automatically transfer all your assets and holdings to their platform. In addition, your relationship with us as your advisor will not change. Our management of your account will continue in exactly the same way as it has done previously. For now, there is nothing that you need to do.

However, one change you will see when the transition takes place is that your current TD accounts will be given a new Schwab account number. For many of you, this will be an irrelevance, but if you have set up any direct deposits from third-party banks, those deposit details will need to be updated with your new account number. Any instructions that you set up via TD Ameritrade will automatically transfer across and won’t require updating.

For a period after the transition (60 days), your deposit instructions will continue to be accepted into your closed TD Ameritrade account and moved to your Schwab account through a residual sweep process. To avoid delays in your transactions being posted, you should update your instructions immediately after September 5, 2023.

After this date, you will also have access to Schwab Alliance, Schwab’s secure online client portal. Just like AdvisorClient (TD’s online portal), Schwab Alliance offers access to account balances, positions, and history, as well as secure online access to statements and tax documents.

If you already have AdvisorClient credentials, you may be given the option to retain them. If you share credentials with another account holder, you will each need to establish credentials to access Schwab Alliance. If you do not have an AdvisorClient.com account, we suggest you create one now.

You will be able to set up these Schwab Alliance credentials approximately one month before the transition date, and you will need either your TD Ameritrade or Schwab account number to do so.

More information about setting up credentials can be found on the Client Learning Center at welcome.schwab.com/alliance or in the Key Information packet, which you will receive in the mail approximately 3-4 weeks prior to the transition.

Many of you use also our direct portal via www.gci-investors.com to monitor your accounts, which will remain unchanged for you.

We will be in touch with another reminder closer to the transition date, and as always, please feel free to reach out to us if you have any questions or wish to discuss any of the above in further detail.

Kind regards,

Guy Davis, CFA

David Shahrestani, CFA

Disclosures: This website is for informational purposes only and does not constitute an offer to provide advisory or other services by GCI Investors in any jurisdiction in which such offer would be unlawful under the securities laws of such jurisdiction. The information contained on this website should not be construed as financial or investment advice on any subject matter and statements contained herein are the opinions of GCI Investors and are not to be construed as guarantees, warranties or predictions of future events, portfolio allocations, portfolio results, investment returns, or other outcomes. Viewers of this website should not assume that all recommendations will be profitable, or that future investment and/or portfolio performance will be profitable or favorable. GCI Investors expressly disclaims all liability in respect to actions taken based on any or all of the information on this website.

There are links to third-party websites on the internet contained in this website. We provide these links because we believe these websites contain information that might be useful, interesting and or helpful to your professional activities. GCI Investors has no affiliation or agreement with any linked website. The fact that we provide links to these websites does not mean that we endorse the owner or operator of the respective website or any products or services offered through these sites. We cannot and do not review or endorse or approve the information in these websites, nor does GCI Investors warrant that a linked site will be free of computer viruses or other harmful code that can impact your computer or other web-access device. The linked sites are not under the control of GCI Investors, and we are not responsible for the contents of any linked site or any link contained in a linked site. By using this web site to search for or link to another site, you agree and understand that such use is at your own risk.

All references and views offered, including but not limited to stocks, companies, investments, investment styles, market returns, expectations, forecasts or estimates and any other area of investing are the opinion of the manager and should not be taken as facts, projections or guarantees. All such opinions are subject to change are do not constitute a recommendation or solicitation to buy or sell a particular security.