Investing vs Speculating: A Gold Story

Gold is in the news again, having soared 34% to record highs in 2020. Is Globescan Capital buying Gold at these levels? No. Not now, likely not ever.

Why not? For the simple reason that we (nor anybody else) really knows what the intrinsic value of Gold actually is. Give us a real asset like a bond or a stock, and we can back out an estimate of intrinsic value based on its expected future cash flows. Give us a bar of Gold, a Picasso, or Dutch tulips, and all we could say is that they are worth whatever someone else is willing to pay for them, which depending on the mood of those individuals, could be higher or lower than yesterday’s price.

This comes back to the fundamental difference between investing and speculating. When you invest, you allocate capital thoughtfully and carefully in assets that you think will generate positive cash flows over time. This involves analyzing the fundamentals of an investment – cash flow profile, risks to that cash flow profile, competition, management, macro factors, etc. This detailed analysis allows us to discover situations where the odds of a good outcome outweigh the odds of a bad outcome. That is investing.

On the other hand, when you speculate, you buy an asset in the sole hope that someone else will pay more for that same asset in the future. Your odds of a good outcome rely entirely on how well you can predict the behavior of other, often irrational, individuals. The asset itself produces no return for you, your only return possibility is from price appreciation. That is speculation, not investment.

Gold: As far from Investing as You Can Get

Buying Gold as an investment is pure speculation. Gold produces no income, no dividends, no cashflow, no return in and of itself. If you buy an ounce of Gold today, in 10 years’ time you will still just have an ounce of Gold. The Gold will not have produced you any extra Gold bars, it will not have produced you any cash. There will not have been any compounding effect.

In fact, the actual cash return of holding Gold is negative; as you have to pay to both store it and insure it. Even if you invest through a Gold fund or a Gold ETF, you still face those same explicit costs, you just will not see them as they’re bundled up with the management fee for the vehicle. But each year, your investment will incur those two very real costs. So, you actually need the Gold price to increase every year just to keep your invested value flat.

Ultimately, the only way to produce a profit here is to hope someone else will be willing to pay more for your Gold, in excess of your holding costs, in the future. We do not know about you, but we would rather not have our investment outcomes be dependent on what the subjective feelings of market participants are towards Gold ten years down the line. We prefer our investment outcomes be dependent on our portfolio companies continuing to produce valuable goods and services at a profit which will be returned to us as shareholders or reinvested internally to produce even more profits.

Exercise: Why is it so hard to value Gold?

We opened this piece by saying that we are unlikely to ever invest in Gold, because we do not know what Gold is really worth- and we don’t think anybody else does either. But as an exercise, let us try to at least attempt to understand what an ounce of the metal should be worth using the most common methods.

To understand the value of any asset, as investors we look at what that asset will be able to generate for us in the future. For stocks this will be the cashflows and earnings that the company will produce in the future, which we as investors own a small percentage of. For bonds it is the coupons we receive. For real estate it is the potential rental income. We calculate this future expected cash flow stream, apply a discount rate based on our confidence or estimation of the risk to those cashflows, and we can arrive at an estimation of the value of that asset.

With Gold, there is no return stream, there is only a net cost each year. So fundamentally, an asset that produces a negative return every year is not an asset, it is a liability. But we must remember that Gold does have some industrial applications outside of just being a vehicle for speculations. Gold is incorporated within some technological and industrial applications, and it is also used a great deal in jewelry. Those two uses of the commodity do mean that the metal itself has some legitimate value. So, if we cannot value it based on cash flow returns and we know it is a commodity metal, then the first step to valuing it should be that which applies to most other commodities.

The price of commodities is set by the economic model of supply and demand. The supply of a commodity is the amount produced each year, whilst the demand is however much people want to buy in order to consume. Where supply meets demand is where the price lands.

However, Gold is importantly different from most commodities for one main reason: very little Gold is ever ‘consumed’. The vast majority of all the Gold that has ever been mined still exists in storage somewhere in the world today. This is not the case with most other commodities: oil gets burned, agricultural commodities get eaten, etc.

The impact of this on the supply and demand picture is very interesting. The World Gold Council (incidentally whose purpose is to “stimulate the demand for Gold”), estimates that so far to date there have been around 200,000 tons of Gold mined in total. This is known as the ‘above ground stock’. To picture this, all the Gold in the entire world would fit in 4 Olympic swimming pools. Each year on average another 2,500-3,000 tons is mined, so the extra amount of above ground Gold increases around 1.25-1.5% per year.

Now, with a normal commodity, the ‘supply’ side of the equation would be this 1.25-1.5% mined each year, that would be the amount available for purchase and consumption. But as Gold isn’t really consumed, it’s mainly just stored; in reality the amount of supply each single year is effectively ALL of the Gold because all of the 200,000 tons above ground is technically available to be purchased at any point in time. And before anyone claims that any Gold stored by central banks in vaults is not available for purchase, remember that ANY asset is available for purchase if the price is high enough. Many banks around the world have and do sell their Gold reserves.

An important implication of this different supply picture is that Gold mining has no real impact on the Gold price. Halting mining for a year or even several years would have such a negligible effect on the supply of Gold that there would likely be no price impact. So, if supply is basically fixed every year, then the only thing that can affect the price is demand. So where does the demand for Gold come from?

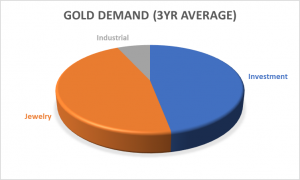

There are three main demand sources for Gold: investment, jewelry, and industrial.

The industrial piece is so small that it cannot really move the needle, so the two important pieces are jewelry demand and investment demand. Interestingly, jewelry demand has been fairly static over a long period of time- it is affected mainly by fashion shifts, and also in response to the price. As the investment piece grows and pushes the price up, Gold becomes less affordable as a jewelry option, so people opt for platinum or silver instead. Just as an aside, the jewelry market is very heavily concentrated in just two countries, with China and India accounting for over half of global jewelry demand.

Given no real impact from technology and fairly stable jewelry demand; in reality the marginal demand comes from the investment buyers and so this is where the price is set. The investment piece includes central bank purchases, which make up around 30% of the investment demand, with the remaining 70% (and therefore the main driver in the Gold price) being pure investment demand. This is made up of asset allocators, investment management companies, Gold funds, Gold ETF’s etc. These are the buyers who really set the price of Gold.

Which brings us back to our opening; the outcome for Gold is unfortunately dependent on what the subjective feelings and possible fear levels of market participants are in the future. As we all know, trying to predict the emotions and movements of thousands of often irrational market participants is never a worthwhile exercise.

However, whilst those movements are not predictable, we can at least try to understand the rationale behind those portfolio decisions. Gold investors typically rely on three main thesis points:

- Gold is a store of value in times of crisis

- Gold is an inflation hedge

- Gold provides negatively correlated returns from stocks

Let us address each in turn:

1- Safe Store of Value

Gold is often touted as a safe haven asset. After all, it has been used as a means of currency for thousands of years and is a ‘scarce’ asset that does not degrade nor decay. Basically, the amount of Gold we have on earth was created millennia ago, and we are not likely to get any more anytime soon. What we have is what we have.

But we must remember that just because something is scarce, does not mean it is valuable. We’ve mentioned before that there’s a limited supply of Globescan branded coffee cups in the world (roughly 4 in our office) but that doesn’t mean we see them as enormously valuable (we are accepting bids).

The next leg to the scarcity argument is regarding the substantial spending by our indebted governments around the world. Surely, when the fiat monetary system collapses under the stress of runaway government debt, we will need a time proven currency like Gold to fall back on?

One argument against this is that the same has been said for hundreds of years and yet there has still been no collapse. If we went back in time 70 years with the complete knowledge that government debt was going to increase more than 400-fold, many Gold bulls would have argued for Gold as an essential part of any portfolio. We now know that would have been a mistake and investors who chose real assets (e.g. stocks) would have done far better.

But let’s for a second ignore history and assume the worst-case scenario; that someday soon our capitalist, fiat money-based society is going to collapse. Buying Gold is often regarded as a fear trade, you benefit if the investment world becomes more fearful.

However, even in this more fearful world, we would argue that one of the last things you would want to end up owning is a lump of inert metal. You would want to own real assets: buildings, trucks, farmland, machinery, guns, canned food, etc. Things that have a use, things that can be used to produce other things.

In this very extreme scenario, some people would also argue that the stock market value would go to zero. But logically this cannot be the case since companies own real assets, and stocks are ownership of those companies. If money loses value, the thousands of trucks owned by UPS will still have a value, because they are still useful assets. The buildings owned by corporations will still have a value, because they can still provide shelter.

In a less extreme and admittedly more likely scenario, the argument goes that traditional currencies will devalue through central bank led inflation or even hyperinflation of the sort that was seen in the Weimar Republic (now Germany) after World War 1. In this scenario it is argued that the most proven and traditional form of currency (Gold) would return as the main currency in use.

That may or may not be true, but it misses the point. A currency is just a means of transaction, it is not an asset in and of itself. It merely exists to represent the value of actual assets. Assets themselves (things that are of use, can be consumed or used to produce other assets) are where the real value lies. You can price them in whatever you want- dollars, euros, Gold, beans, sheep, etc. The currency itself is not what protects you, the protection comes from the actual asset itself. So, we need to worry less about the currency, and worry more about what the actual assets we own are.

2- Inflation Hedge

Gold bulls argue that the magical metal will protect you against both inflation AND deflation. They will pick snippets of time that show that Gold has outpaced inflation over specific periods historically. For example, just look at the 1970’s, when Gold’s performance matched that of double-digit inflation. Or look at the last 100-years as Gold has held its value while the dollar steadily declined. But what they will not tell you is to look at the many periods, like the 20 years from 1980 to 2000, when the Gold price fell 80% whilst inflation doubled.

And what they definitely won’t tell you is that, while it is true Gold outperformed the dollar over the last 100-years, it is not true that Gold outperformed the U.S. stock market. The reason for this is quite clear when we think about it logically. In a world of rising prices (inflation), would you be better off holding a useless bar of Gold, or a productive enterprise that generates products and services that are in demand? The best inflation hedge will always be a business with pricing power, which can raise prices to match inflation, preserving the purchasing power of its investors.

3- Diversification from Equities

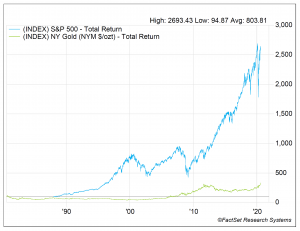

This is the arguably the most outlandish and unfounded of the Gold bull claims – after all, why would you want to diversify away from consistently making money? Just bury 10% of your net worth in the back yard and there, you have diversified away from the ‘risk’ of the equity markets. The problem is that you’ve also diversified yourself away from the returns of the equity markets. Consider that for most people, the bulk of their investing lives takes place over around a 40-year period. Over the past 40 years, gold has returned roughly 400% while the S&P 500 has returned roughly 3000%.

In fact, you would be hard pressed to find any substantial period where Gold outperformed equities, even more so if you were looking at risk adjusted terms. It is important to highlight that fact: not only has Gold vastly underperformed the stock market, it has done so with far higher volatility. As a Gold investor, rather than as a stock investor, you should expect lower returns with much more extreme price swings.

However, this is a long- term view of the world, and we accept that there are short term reasons why some investors may need to diversify their equity risk. This again comes back to the fear trade: in times of equity market weakness there is the expectation that investors flock to safe haven assets such as treasury bonds or Gold. Looking back through history and there have certainly been times when Gold has been negatively correlated with stock returns, and thus would have provided protection.

But there is a huge problem: there have also been numerous periods where Gold was positively correlated and fell at exactly the same time as stocks. And some of those times, have been the times when you needed protection the most: The Financial Crisis in 2008, and also the 2000 tech bubble are two notable examples. As a result, investors simply cannot rely on Gold providing any form of diversification or protection from equity market returns. Right now, many people are calling for Gold as a diversifier on the basis that the S&P 500 is within a few percentage points of its all-time highs, but that argument quickly falls apart when you realize that right now Gold is also within just a few percentage points of its all-time highs…

Unfortunately, the simple fact is that there is no consistent relationship between Gold and the stock market. As a result, Gold cannot be relied upon as a reasonable and reliable hedge for stock portfolios. We prefer that our investment outcomes are dependent on our portfolio companies continuing to produce valuable goods and services at a profit which can be returned to us as shareholders or reinvested internally to produce even more profits.

Disclosures: This website is for informational purposes only and does not constitute an offer to provide advisory or other services by Globescan in any jurisdiction in which such offer would be unlawful under the securities laws of such jurisdiction. The information contained on this website should not be construed as financial or investment advice on any subject matter and statements contained herein are the opinions of Globescan and are not to be construed as guarantees, warranties or predictions of future events, portfolio allocations, portfolio results, investment returns, or other outcomes. Viewers of this website should not assume that all recommendations will be profitable, or that future investment and/or portfolio performance will be profitable or favorable. Globescan expressly disclaims all liability in respect to actions taken based on any or all of the information on this website.

There are links to third-party websites on the internet contained in this website. We provide these links because we believe these websites contain information that might be useful, interesting and or helpful to your professional activities. Globescan has no affiliation or agreement with any linked website. The fact that we provide links to these websites does not mean that we endorse the owner or operator of the respective website or any products or services offered through these sites. We cannot and do not review or endorse or approve the information in these websites, nor does Globescan warrant that a linked site will be free of computer viruses or other harmful code that can impact your computer or other web-access device. The linked sites are not under the control of Globescan, and we are not responsible for the contents of any linked site or any link contained in a linked site. By using this web site to search for or link to another site, you agree and understand that such use is at your own risk.