First Quarter 2021 Update

Dear Clients,

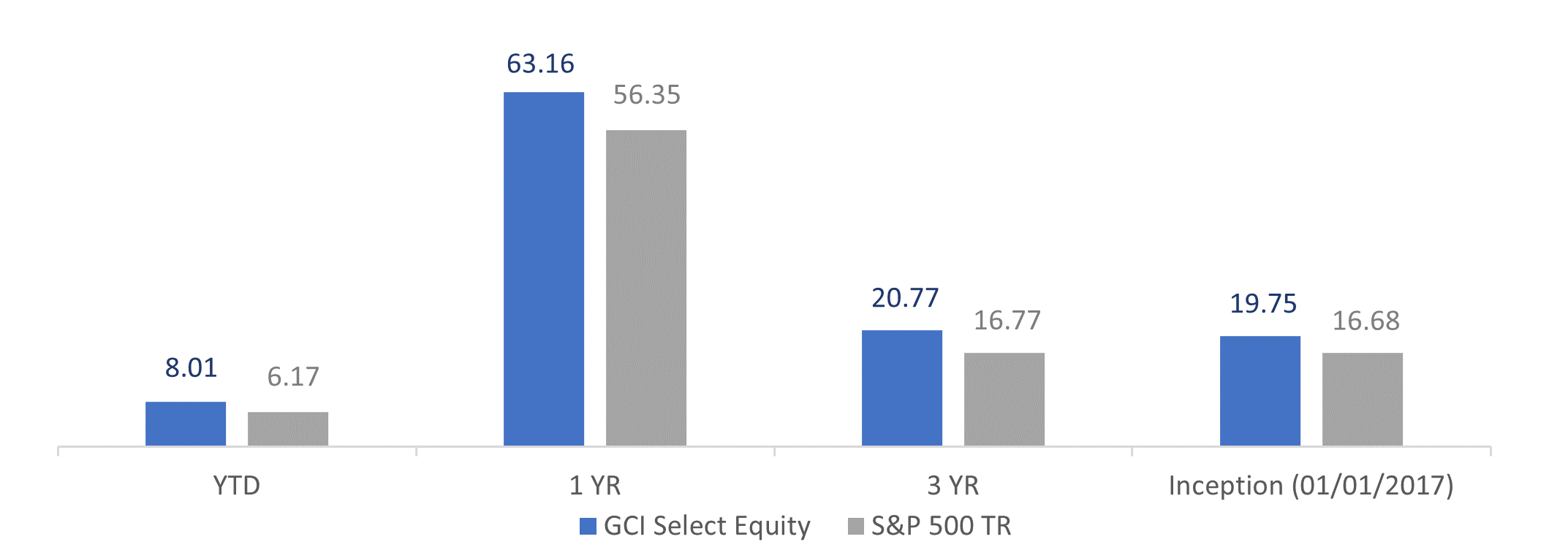

We are pleased to report another positive quarter in both absolute and relative terms. Our GCI Select Equity strategy ended the first quarter of 2021 up 8.01% gross of fees. For comparison, the S&P 500 ended the quarter up 6.17%.

Over a trailing three-year period, our strategy has now compounded client capital at a rate in excess of 20% per annum, and since the Covid-19 lows a year ago the strategy has risen roughly 60% – a testament to the advantages that come with having a long-term focused client base, allowing us to ride out periods of volatility when other managers might be forced to panic sell.

Over a trailing three-year period, our strategy has now compounded client capital at a rate in excess of 20% per annum, and since the Covid-19 lows a year ago the strategy has risen roughly 60% – a testament to the advantages that come with having a long-term focused client base, allowing us to ride out periods of volatility when other managers might be forced to panic sell.

Despite these positive results, you will likely have noticed that in a number of our recent articles we have been calling out why a prudent, long-term investment strategy, such as our own, will at some point start to underperform a broader market that is in a speculative boom. After all, if it did not then it wouldn’t be a prudent strategy – it would simply be taking ever-more risk to chase ever-lower returns.

The timing of these articles has been no accident. For the last few months, we have begun to see some pockets of irrational exuberance forming in the market. As we have seen these pockets emerge, our preferred strategy has been to simply avoid them, and instead focus on where we can find more defensible value for the long run.

As you know, Globescan Capital was founded on the principle that investing in high-quality companies at attractive prices is the most durable and consistent way to achieve long-run, risk-adjusted returns. As such, we will continue to do just that, even when the rest of the industry is shifting its focus to more “get rich quick” schemes.

The problem with these short-term strategies is that they often ignore the most fundamental concept in investing: that there is a difference between the price of something and its value. In the short run, investors might feel vindicated as they see the price of their holdings go straight up, but just because the price is going up, does not mean that the value is going up. In the long run, value is the measure that always wins out.

We have written about this issue many times before but given some of the extremes we are seeing in the markets today, we thought it would help to expand on our thinking with some timely examples.

Price Versus Value

Firstly, we need to begin by explaining what we mean by “Price” and “Value”. Price refers to the quoted cost of any share on any given day, whereas value refers to what a shareholder receives in exchange for paying that price – the value inherent in the company, often defined as the present value of all the future cash flows that are going to be available for distribution to shareholders.

In simpler terms: price is what you pay, and value is what you get.

Thus, any prudent investment strategy will seek to buy businesses where the value (future cash flow potential) is greater than the price paid (current cost of ownership). While this strategy may seem painfully obvious in theory – in practice, it features little in most investment approaches, as it can only be successfully applied with a long-term horizon. Sadly, that has increasingly excluded most of the industry where the focus has shifted to pushing ever-more lucrative (for Wall Street) short-term trading strategies onto retail clients.

To help expand on why Price and Value are so important, we are going to talk about both from three different perspectives: 1) an asset with a price but no value (Bitcoin, gold, art, etc.), 2) an asset with both a price and a value but where the value being overwhelmed by the price in the short run (GameStop in Q1), and 3) an asset with a price and value where the price is being overwhelmed by the value in the long run (Amazon over the past 15 years).

Price Without Value: Bitcoin

Bitcoin, gold, art, collectibles, etc. are all examples of non-cash flow producing assets. In other words, things that have a price, but no intrinsic value to anchor that price to. As such, they are worth whatever others are willing to pay for them in a supply and demand driven market.

Any trading in such “assets” is by its very definition an exercise in speculation – buyers wishing to be rewarded with price increases in return for generating nothing of value. A kind of zero-sum game.

For example, let us focus on Bitcoin. The most recent iteration of the bull case for Bitcoin (there have been many that didn’t pan out) is that it is a store of value, akin to being a new digital-based gold. We use the term “value” here loosely, referring not to the cash flows generated for Bitcoin holders, or any products and services generated for society, but to the preservation of purchasing power over time.

It seems obvious to us that the real reason most large institutional and retail buyers alike have bought into Bitcoin is not to preserve future purchasing power, but to make a profit. After all, “preserving purchasing power” is about as unexciting an investment strategy as it gets – it just means you are staying stagnant in real wealth terms. Instead, holders of Bitcoin expect that their purchasing power will increase over time, they expect to get rich.

And consider that after years of innovation in the space, little overall value or societal benefit has been created by Bitcoin at all, instead most of the innovation around the space has been in creating ever-more casino like structures to further speculate on the price of cryptocurrencies.

Contrast this zero-sum speculation with an equity investment in a company like Apple which has created real value. Apple largely invented the mass market concept of a smart phone, an idea that has led to a computer in almost everyone’s hand. That innovation has created an enormous amount of value for Apple as a company, but also far more value for society than Apple will ever be able to capture for themselves or their shareholders. There is nothing zero-sum about what Apple has created for the world.

So, with Bitcoin we are left with an asset that trades on pure speculation with no underlying value to justify if it is overvalued or undervalued on any given day. We avoid it and other speculations for just that reason. But going one step further, we also see much of the time and energy that has gone into the space in the name of “investing” as a tremendous waste. After all, shouldn’t we be encouraging investment in productive assets that benefit society, and discouraging the hoarding of any metal or currency?

Price Overwhelming Value: GameStop in the Short Run

The next example is of those assets that do have a value, but where that value is largely disregarded in order to trade it in the short run based solely on price. The first quarter of 2021 was characterized by some very high-profile examples of this, where stock prices increased by hundreds of percent in a matter of days – GameStop being the one that got the most news attention, but there was also AMC, VIAC, a bunch of SPAC’s, etc. We all know that the fundamental value of a business rarely doubles or triples in a few days, so what was going on?

In the short run, price is a function of supply and demand; which is influenced by short-term news flow and liquidity. This has always been the case and will probably only become more the case over time along with the rise of passive investing and the effect that social media has had on amplifying short-term narratives.

GameStop was a great example of this – a combination of social media buzz creating demand that an illiquid supply (small float) could not keep up with. More buyers than sellers mean that the stock price goes up (particularly in a short squeeze). However, such price movements bear no correlation to changes (or the absolute level of) the underlying value of a business.

Could we have made money riding GameStop to nearly $500 and then exiting before the crash? Possibly, but we definitely couldn’t do it consistently and we don’t think anyone else could either. To say that you can predict the short-term supply and demand balance for any stock consistently is to say you can predict not only thousands of variables, but also how (often irrational) market participants will react to those variables. It just is not possible.

So, with GameStop, we were left with an asset trading solely on price with no regard for value. This is a dangerous game since when you disconnect price from value you end up with a situation (like with Bitcoin) where speculation could easily see the price double or halve in a given day. As such, we avoid these speculative frenzies.

Value Overwhelming Price: Amazon in the Long Run

Unlike either of the first two examples, with a long-term investing strategy such as ours, we take almost the opposite approach – we can largely ignore the unpredictable price side of the equation (outside of it providing us with opportunities to transact) and instead focus on the more predictable and important value side of the equation – a business’s underlying ability to generate cash flows for us as investors.

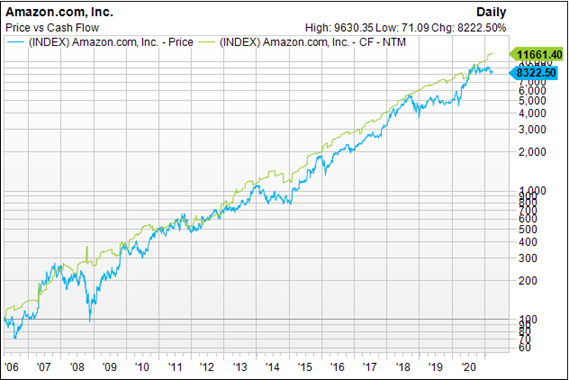

The great thing about this strategy is that over the long run value has always been and will always be the main determiner of investment returns. For example, consider the last 15 years of price returns for a company like Amazon relative to its last 15 years of operating cash flow growth:

The blue line represents price, and the green line represents value. Notice the volatility of the blue line – during this period, the price of Amazon experienced multiple 30% moves down, as well as a large 65% drop during 2008. Any investor that solely focused on the blue price line during this period likely felt compelled to abandon the investment entirely during any of these significant drawdowns.

Yet during this same period, the underlying cash flow generative ability of Amazon continued to tick upward. In other words, the real value of the company continued to compound despite what the price was telling you. For any investor solely focused on the green value line, the ride was much smoother and more predictable. And more importantly, instead of abandoning the investment during any given price drawdown, they would instead likely be adding to the position.

This is what investing is all about: focusing on real intrinsic value and transacting only when price offers opportunities. This has been and always will be our approach.

Portfolio Changes

During the first quarter, we initiated a new position in GFL Environmental – a waste disposal company based in Canada. Led by dynamic founder Patrick Dovigi, GFL stands at the beginning of a significant runway of industry consolidation in what has traditionally been a somewhat sleepy, fragmented marketplace. For further information, we will provide an abridged version of our investment thesis in a future article.

As always, we thank you for partnering with us. Please feel free to reach out with any questions or comments you may have.

Best regards,

Guy Davis, Pas Sadhkuhan, Shaumo (Neil) Sadhukhan, David Shahrestani

Disclosures: This website is for informational purposes only and does not constitute an offer to provide advisory or other services by Globescan in any jurisdiction in which such offer would be unlawful under the securities laws of such jurisdiction. The information contained on this website should not be construed as financial or investment advice on any subject matter and statements contained herein are the opinions of Globescan and are not to be construed as guarantees, warranties or predictions of future events, portfolio allocations, portfolio results, investment returns, or other outcomes. Viewers of this website should not assume that all recommendations will be profitable, or that future investment and/or portfolio performance will be profitable or favorable. Globescan expressly disclaims all liability in respect to actions taken based on any or all of the information on this website.

There are links to third-party websites on the internet contained in this website. We provide these links because we believe these websites contain information that might be useful, interesting and or helpful to your professional activities. Globescan has no affiliation or agreement with any linked website. The fact that we provide links to these websites does not mean that we endorse the owner or operator of the respective website or any products or services offered through these sites. We cannot and do not review or endorse or approve the information in these websites, nor does Globescan warrant that a linked site will be free of computer viruses or other harmful code that can impact your computer or other web-access device. The linked sites are not under the control of Globescan, and we are not responsible for the contents of any linked site or any link contained in a linked site. By using this web site to search for or link to another site, you agree and understand that such use is at your own risk.