First Quarter 2022 Update

Dear Partners,

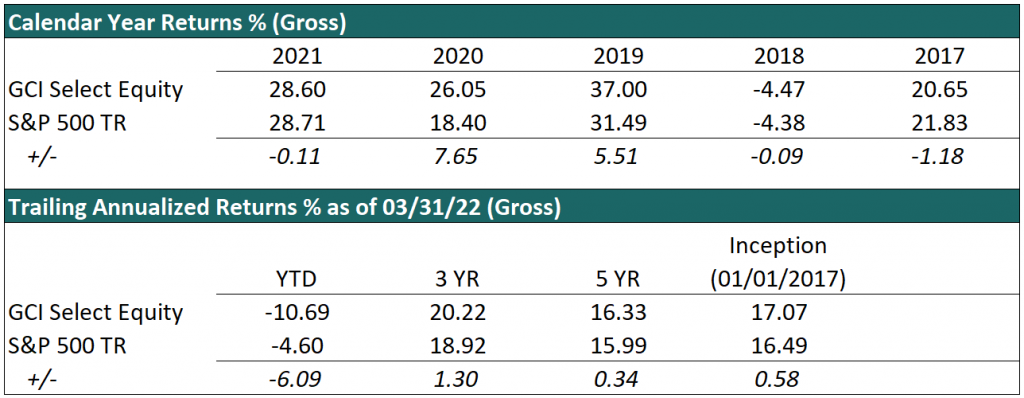

Our GCI Select Equity composite ended the quarter -10.69% gross of fees. For context, the S&P 500 ended the quarter -4.60:

Underperforming the market is never welcome, but over such a short period of time is of little consequence. We at GCI focus on providing long-run outperformance by investing in a concentrated portfolio of high-quality businesses at attractive prices. We do not focus on outperforming the market over every reporting period, nor trading in and out of whatever is currently in favor.

This disciplined approach often means going against the grain in the short term. For example, we aren’t going to invest in businesses like AMC Theatres or GameStop just because they outperformed this quarter, nor are we going to invest in commodity businesses just because geopolitical events created a short-term spike in commodity prices. In each case, these have not magically become high-quality businesses just because their stock prices have gone up recently.

Furthermore, as far as current events and market timing, you will likely have read in the news that both the significant drop we have seen in the markets this year, as well as the recent recovery, can both be explained by some combination of inflation, interest rates, the war in Ukraine, or various other hindsight-led reasons. In fact, it has been a great reminder to us how futile short term market attribution can be, as we have often found ourselves presented by the news with the exact same explanation for both market rises and market falls.

In reality, nobody knows why the market does what it does in the short term. The market is a complex system of human (or human programed) actors and anyone trying to predict the short term is simply engaging in a futile version of the Keynesian beauty contest in which they try to guess how other market participants will react to news, who in turn are trying to guess how other market participants will react to news, and so on, and so on.

We simply avoid this misguided effort and instead focus our attention solely on the moat-protected free cash flows that we expect will be produced by our portfolio companies over the course of years, not days. This approach not only insulates us from the noise and distraction of day-to-day share price volatility but also turns that volatility into opportunity – allowing us to buy or sell companies as their market pricing becomes un-tethered from their underlying business value.

Portfolio Commentary

One of our worst performers in the quarter was Ocado Group (OCDDY) with its stock price down roughly 33%. Despite this significant share price movement, we remain comfortably optimistic for future returns as the business has continued to compound its value.

Consider that today Ocado’s shares have been sold off by the market along with a group of so-called ‘Covid-19 beneficiaries’ in the home delivery space (DoorDash -20%, Just Eat -38%, Instacart -38%). Does this grouping make sense? We would argue that many of these other companies have economically nonviable solutions compared to Ocado’s proven automated centralized fulfillment technology.

Then consider that as far as underlying business value goes, Ocado has continued to win and expand partnerships – yet in each case the ramp up time for these centralized fulfillment center (CFC) deals can take years, meaning Ocado faces expenses to construct these CFCs today, but does not receive the majority of the economic benefit until years later.

As the market tends to be short-term in nature, it hates these kind of arrangements. But for us, with a rational long-term horizon, we can look at the unit economics of each CFC development that Ocado is currently spending money on today. Doing so, we can see the likelihood of 40% returns on capital once these CFCs ramp up. There aren’t many companies with a long runway to invest at 40% returns, and as such, we are very happy to continue to own Ocado at these discounted levels.

A similar story can be seen in GFL Environmental (GFL) which was down 14% in the quarter and is now one of our largest holdings after adding during the weakness.

At its core GFL is a simple business – they operate trucks that collect and dispose of waste. Now, the waste collection and disposal industry has historically been a stable one where volumes grow roughly along with population growth, plus some reasonable pricing power which results in overall organic growth in the mid-single digits. When it comes to the waste collection side of things, this industry is protected from competition through route-density based economies of scale, and on the disposal side by very hard to re-create fixed investment in landfills.

GFL then benefits from further upside relative to its publicly traded industry peers (WCN, WM, and RSG) in that GFL has a more attractive M&A runway. At GFL’s size, rolling smaller independents into their network results in significant scale advantages, driving long-term margin expansion while naturally deleveraging their balance sheet over time. In addition to this more attractive runway, we would also argue that GFL has the best and most shareholder aligned management in the space.

Despite all this, GFL has underperformed their less exciting peer group by roughly 12% in the quarter, even after already having started at a relative discount. In our view, the market is incorrectly punishing GFL – there is a long and stable runway for GFL to continue compounding their cash earnings at mid-to-high double digits, and as such, we were happy to add to our position.

Thank You

As always, we would like to take this opportunity to thank you, our partners for your continued trust in us and our approach.

After all, the success of any investment strategy depends on a mutual understanding between us as the manager, and you as our investors and partners on what our ultimate goal is and how we intend to achieve it. As such, we recently published an Owner’s Manual for the strategy which further expands on these ideas. It can be found at the following link:

https://genuineinvestorsetf.com/gcig/owners-manual

Please feel free to reach out to us with any questions you may have, or if you would like to discuss any of this further.

Kind regards,

Guy Davis, David Shahrestani, Pas Sadhkuhan, Shaumo (Neil) Sadhukhan

Disclosures: This website is for informational purposes only and does not constitute an offer to provide advisory or other services by GCI Investors in any jurisdiction in which such offer would be unlawful under the securities laws of such jurisdiction. The information contained on this website should not be construed as financial or investment advice on any subject matter and statements contained herein are the opinions of GCI Investors and are not to be construed as guarantees, warranties or predictions of future events, portfolio allocations, portfolio results, investment returns, or other outcomes. Viewers of this website should not assume that all recommendations will be profitable, or that future investment and/or portfolio performance will be profitable or favorable. GCI Investors expressly disclaims all liability in respect to actions taken based on any or all of the information on this website.

There are links to third-party websites on the internet contained in this website. We provide these links because we believe these websites contain information that might be useful, interesting and or helpful to your professional activities. GCI Investors has no affiliation or agreement with any linked website. The fact that we provide links to these websites does not mean that we endorse the owner or operator of the respective website or any products or services offered through these sites. We cannot and do not review or endorse or approve the information in these websites, nor does GCI Investors warrant that a linked site will be free of computer viruses or other harmful code that can impact your computer or other web-access device. The linked sites are not under the control of GCI Investors, and we are not responsible for the contents of any linked site or any link contained in a linked site. By using this web site to search for or link to another site, you agree and understand that such use is at your own risk.