Fourth Quarter and Full Year 2021 Update

Dear Partners,

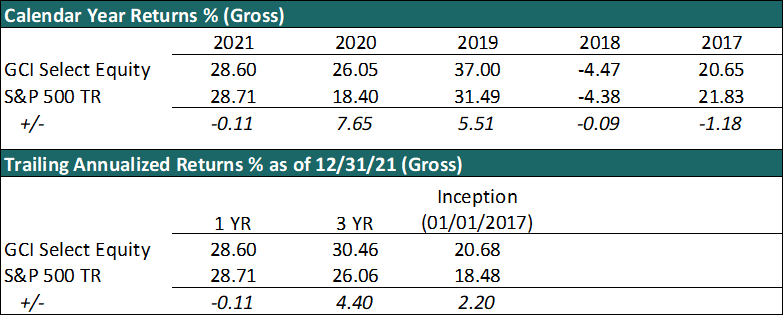

We are pleased to report another positive year of absolute performance with our strategy (see product page) up 28.60% gross of fees.

Individual separate account performance may differ based on asset mix and timing of investment- the above numbers are for the strategy composite as a whole.

Individual separate account performance may differ based on asset mix and timing of investment- the above numbers are for the strategy composite as a whole.

You will have likely noticed that we spent much of this past year cautioning that if the market continued to go straight up with no regard for underlying fundamentals (which it then did) then a prudent, long-term strategy such as our own could start to underperform that market over the short term.

Despite that cautioning, we still managed to end the year within a hair’s breadth of the S&P 500 – an increasingly flawed, but common proxy for the overall market. We only bring this up as a reminder that we should all be largely indifferent to short-term relative performance for several reasons:

- Considering the concentration of our portfolio (23 positions vs 500 positions for the S&P) it is surprising that we are anywhere near the S&P at all,

- On a risk-adjusted basis, we are still far more comfortable holding our 23 businesses than owning an arbitrary list of 500 businesses ranked based on popularity, which includes many sectors we find structurally unattractive from an investment perspective and most importantly,

- We measure our success not by how much our holding’s stock price has changed in a single year, but by the appreciation of the look-through cash earnings that our holdings generate for us, and the outlook for those earnings going forward. In other words, we measure our success by how the actual businesses we own are performing.

As you know, GCI was founded on the principle that Genuine Investing is the most consistent way to achieve long-run, risk-adjusted returns. And Genuine Investors make investments in businesses, not speculations in stock prices.

It is true that there are many investment managers that have on occasion delivered high returns (usually with hidden risks) running strategies that are more akin to speculating in stocks – investing in fads, themes, momentum, arbitrage, etc. We are not one of those managers. Instead, we seek to invest in the purest sense – allocating capital to great businesses at reasonable prices and then letting those businesses compound their value over time.

As we enter 2022, we would like to take this opportunity to thank you, our partners, for your continued loyalty and trust which allows us to execute on this strategy. We have said it before and we will say it again, we are very fortunate to have the client base that we do.

Looking Back at 2021

We like to spend these updates talking about what matters most for our future performance – the companies we hold. That said, we would be remiss if we didn’t spend a little bit of time discussing some of the exuberant behavior observed in the market this past year and some lessons we might glean.

In 2021, the S&P 500 ended the year up 28.71%. We have talked before about how the S&P is becoming less representative of the economy, increasingly risky and momentum based, and more a proxy for how large cap tech is performing. Namely – Apple, Microsoft, Amazon, Tesla, Alphabet, and Meta Platforms which make up nearly 25% of the index. What started years ago as an index of the 500 largest companies trading in the US has morphed into a popularity contest where a company like Tesla outranks all other auto-manufacturers combined.

There are significant implications of this. For example, the headline S&P number masked a lot of pain elsewhere in the market. Consider that nearly 40% of the stocks in the Nasdaq Composite are now down 50% from their highs and two thirds are down at least 20%. Zoom, after rallying five-fold in 2020, saw its share price crater nearly 70% from its highs. Peloton, after rallying five-fold in 2020, saw a fall of nearly 80% from the highs. Popular growth ETF ARKK is now down 50% from the highs.

This all serves as another reminder of the dangers of so-called momentum strategies, and Wall Street’s habit of often taking whatever has recently been working and projecting that continued success well into the future. In reality, competitive forces can change quickly in industries and underwriting investments without a margin of safety to account for this fact can be disastrous.

Elsewhere in 2021, we saw the rise of so-called “Meme” stocks – characterized by a complete (and often proud) disregard of the underlying business and instead a myopic focus on the ‘stock’ as an independent entity- with the hope that a speculative frenzy could lead to an exit at a higher price. The greater fool theory of investing. We are of course referring to names like GameStop, AMC Theatres, Hertz, etc.

We don’t have much to add to the record on these specific names, other than noting this is an interesting social experiment bending the rules of capitalism – we now have numerous companies who remain in existence purely due to the proud irrationality of an online mob, companies which under normal circumstances would long ago have succumbed to ‘survival of the fittest’ and either folded entirely or needed heavy restructuring.

But aside from the interesting academic experiment, such examples do raise an important point around the difference between speculation and investment.

When speculating, you can only make money if someone else pays more for your position in the future. For example, buying a meme-stock and then selling it to someone else at a higher price. Nothing new was created from this transaction, no growth at the company, no increased earnings for shareholders, simply a change in stock price. A common error that those who subscribe to this line of thinking make is believing that wealth comes from scarcity – if I have the scarce asset and you don’t, then I hold the wealth. Examples of this are rife in today’s world: gold, bitcoin, NFTs, etc.

In reality, wealth comes not from scarcity or speculation but from abundance in productive capacity. The reason we have a higher standard of living today than the kings of old is not because we have more gold bars than they did (nor because someone invented cryptocurrency), but because our economy has more productive capacity – we invested in the past to have more abundance today. As such, societies get richer not by making speculations, but by making real investments in the future.

As such, we would only hope that much of the time and effort spent this past year speculating on meme-stocks and cryptocurrencies finds its way towards better uses in the years to come.

After all, it is real underlying businesses that will drive both our performance as well as economic growth. Market prices only matter in so much as they provide us the opportunity to transact. As such, let’s spend the remainder of this letter discussing a few of our notable portfolio holdings this year:

Meta Platforms (FB)

Meta Platforms, formally known as Facebook, has been in the news at lot this year due to both political backlash (nothing new) as well as due to a complete rebranding of the company (that is new).

Our core thesis here is unchanged – Mark Zuckerberg is still one of the best capital allocators of our generation, the core advertising business is growing 30%+ even with supply chain and iPhone advertising targeting headwinds, and there continues to be the opportunity to monetize under-monetized assets (think WhatsApp, Shops, etc.). And we believe we get all of this for much less than the company is worth, with the discount stemming from much of that negative news flow mentioned above.

However, we do believe the downside risk here has changed over the past year – where a year ago the main risk to the business was regulation, today there is a significant amount of capital spending occurring with less obvious returns than the core advertising business.

Consider that FB is currently guiding for $29B-$34B of capital expenditure, as well as $10B of accelerating operating expense in 2022 for their VR/AR (virtual reality/ augmented reality) segment. To put that into perspective – Google loses roughly $5.6B on their other bets versus revenue of $250B (2%), FB’s $10B “other bet” is 8%+ of their revenue. On the capital expenditure side, in 2020 one of the most capex heavy companies around: AMZN, spent $50B on capex + finance Leases, and yet FB is spending $34B for what is supposed to be a capital light business model. It even dwarfs traditional capex heavy companies: Exxon spends $17B, Taiwan Semiconductor is spending $30B.

Now, we have already said that we believe Mark Zuckerberg is one of the best capital allocators of our generation, but how much of this huge investment in VR/AR is arguably a result of 1) FB not being allowed to do any more acquisitions, and 2) a kneejerk reaction to Apple pressures. Effectively the cash FB generates must go somewhere, and if FB is not allowed to acquire other businesses, and they don’t want to show huge profits to attract even more political attention, reinvesting it in product development seems like the only option left. That would be the cynical view, and certainly one that warrants consideration.

However, we believe the strategy from FB here seems to be that there is a window of opportunity to get a first mover advantage on the next generation computing platform shift. It is not a given that FB will be successful, since we must remember that Apple and Microsoft (as well as many smaller competitors) are going after the same market, each with competitive advantages of their own. But it is probably worth a try considering the amount of upside optionality they are receiving.

Ultimately, there is really no way to reliably determine what the returns on FB’s investments into VR/AR will be. So, as Genuine Investors, we must discount a lot of the hype around these investments and instead focus on the core value that we are receiving in return for allocating our capital to FB – which we still believe is a lot. We are getting core FB at such a discount that it more than makes up for any value that we can conservatively estimate could be burned away trying to bring VR/AR to life. We will continue to monitor the company to make sure that remains the case.

Air Products (APD)

We often talk about the fact that some industries just aren’t very attractive for investment (commodities, pharmaceuticals, etc.), but there are others that have fundamentally attractive attributes. The industrial gasses industry is one of those. As a reminder, Air Products build, own, and operate large scale gasification plants that produce gasses (oxygen, nitrogen, hydrogen, etc.) for use in a variety of different end markets. Substantial amounts of gas are required in a wide (and increasing) variety of industrial processes: steel production, oil refining, food processing and medical applications, as well as huge nascent future trends such as hydrogen mobility.

For many large-scale industrial applications, APD will build a multi-billion-dollar gasification plant at a customer’s production site. This is a tremendous value proposition: the customer shares the cost of the build and then commits to a minimum volume on 15-20 yr. ‘take or pay’ contracts. Air Products can therefore make substantial capital investments with high visibility over their long-term returns. Such a proposition is rare in the investing world. These large-scale plants make up over half of APD’s earnings, with another third coming from ‘bulk’ gas and liquid – this is truck load sizing delivery rather than on site plants, a business line that also comes with reasonably good contract terms, typically 3-5 years.

Under the leadership of Seifi Ghasemi, Air Products have put themselves in an enviable position over the last 5 years. While their main competitors are over-levered following acquisitions, APD have been sitting with net cash, giving huge capacity for investment. This was the situation entering 2020, and as we progressed through 2021 several opportunities that management have been working on for some time began to take shape. The company began signing deals and putting shovels in the ground on new projects.

This resulted in a big jump in capex, something the market almost always dislikes in the short term, as it’s too myopic to recognize the future benefits. APD added 2,000 engineers during 2021, and they committed all of the $18bn of investment capacity they announced back in 2018. In total, they will be deploying around $30bn of capital over the next 8 years. Given the extreme focus APD have on returns, we can be reasonably comfortable that this capital is going to good use, and it sets us up well for the future.

The share price has lagged the market this year, but the business returns and fundamentals have been excellent, and we are in a far better position as shareholders than we were last year given the future returns we expect. The value that APD shares represent is greater now than a year ago.

Ocado (OCCDY)

A new position for us this year, though a company that we have known and followed closely for many years, Ocado is the only ADR (American Depository Receipt) we hold – a 2 for 1 fungible ADR with the main London listed line, OCDO. There are very few world class companies that are based in the UK, and Ocado is one of them.

As you know, our preference in investing is for as few things to go wrong as possible – the fewer the variables we have to forecast, the lower the chance of significant errors. Ocado is a company that is clearly leading the world in one of the most sure-fire industries that exists: online grocery delivery.

For the customer, grocery delivery is a far more attractive prospect than most other forms of online delivery, even those which have already proved popular. There are several reasons for this: because the basket sizes are far larger (number of items) which means it takes longer to shop for, it’s also therefore inherently harder to carry, and finally because you typically end up buying the same things week in week out.

And yet bizarrely grocery delivery is still only 11% of total shopping in the US, far behind other forms of online retail. The simple reason is that delivering groceries is very difficult to do profitably. And as a result, supermarkets have tried to do as little of it as possible. Most grocers earn little more than 2-4% operating margins, so they have little capacity for loss making operations. Many companies have tried to tackle this problem and make it profitable, so far Ocado are the only company to do so at scale.

When you compare delivering food, to delivering most other goods that we buy online, you encounter 3 very significant complications, which have so far meant that even the best logistics companies in the world (including Amazon) have failed to do online grocery delivery profitably:

- Perishability: food goes bad, often quickly. Meats, fruits and vegetables have varying and often short shelf lives.

- Temperature zones: you have to deal with ambient, chilled and frozen foods. They need to be stored, packed and delivered in their correct zones to ensure freshness.

- Basket size: your average online shopping order is only a couple of items. Your average grocery basket contains multiples more individual items.

Ocado have solved this problem, having been focused entirely on it for the last twenty years. But the real key to understanding Ocado is not that they are just a very efficient online grocer, but that they can take their already proven technology and sell it to other grocers. So, the ‘product’ Ocado is selling is really their self- titled ‘Ocado Smart Platform’ – a modularised combination of hardware and software to enable online grocery for traditional supermarkets. Ocado licenses, installs and operates the technology, and then they share in the ultimate revenue pass through. This is an incredibly scalable business model and one where they face few legitimate competitors. As a result, in the last two years Ocado has signed deals with grocers in Canada, US, Sweden, France, Australia, Japan and the UK. Most of these deals are just at the capex stage, yet to be fully operational. In the US, they signed a huge deal with Kroger and are building out the Kroger online platform across the US. Kroger even took a 5% equity stake in the company. With all of this build out around the world, we sit right at the beginning of what should be a tremendous decade of growth for the company.

Despite this incredibly runway in front of us, we’ve been offered some excellent buying opportunities this year, as the stock has been swung around with lockdown/ re- opening trades. A great example of short termism benefiting the Genuine Investor.

As always, we welcome discussion and your thoughts.

Kind regards

Guy Davis, David Shahrestani, Pas Sadhkuhan, Shaumo (Neil) Sadhukhan

Legal Disclaimer: This document expresses the views of the author as of the date indicated and such views are subject to change without notice. Globescan Capital, Inc. is DBA as GCI Investors, and has no duty or obligation to update the information contained herein. Further, Globescan Capital, Inc. makes no representation, and it should not be assumed, that past investment performance is an indication of future results. Moreover, any information or opinions contained in this document are not intended to constitute a specific recommendation to make an investment.

The information contained herein does not constitute and should not be construed as an offering of advisory services or an offer to sell or solicitation to buy any securities or related financial instruments in any jurisdiction. Certain information contained herein or linked to is based on or derived from information provided by independent third-party sources. Globescan Capital, Inc. believes that the sources from which such information has been obtained are reliable; however, it cannot guarantee the accuracy of such information and has not independently verified the accuracy or completeness of such information or the assumptions on which such information is based.