Third Quarter 2021 Update

GCI Select Equity Q3 2021

Dear Clients,

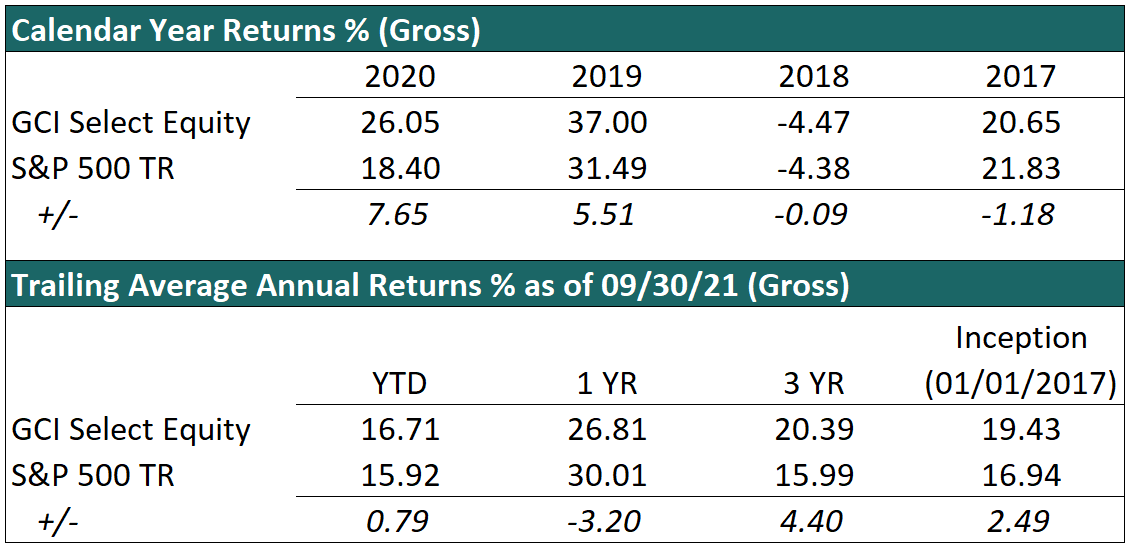

We are pleased to report that our GCI Select Equity strategy ended the third quarter of 2021 up 16.7% year-to-date (gross of fees).

As you know, we spend little time discussing short term performance as it is not helpful in measuring a long-term strategy such as our own. So, while short-term performance remains positive, we always maintain that the best yardstick to measure us by is our long-term results where over the past three years, our equity portfolio has averaged 20% per year gross of fees, vs the S&P 500 at just under 16%.

GCI was founded on the principle that investing in high-quality companies at attractive prices is the most durable and consistent way to achieve long-run, risk-adjusted returns. Despite whatever happens with the overall market in the short run, we will continue to do just that.

As a team, we have put in significant work over the past few years to better communicate this concept. You have probably noticed this effort in many of our articles, and most recently in our book Navigating the Street: A Better Approach to Investing. We strive to be very transparent in our process – we feel that you, as our clients, should feel comfortable and informed about what we own and more importantly why we own it.

It is important that we spend time on this because our approach is very different from most of the investment industry as it exists today, despite our approach having its roots in ideas that have existed for decades. Today’s investment industry is dominated by by passive, factor, thematic, macro, crypto and meme, investing. Our approach is very much an outlier in this group.

So, we have been working for some time on the best way to convey our approach simply and concisely, and to do so we would like to introduce to you the concept of “Genuine Investing”.

What do we mean by Genuine Investing? At its simplest – Genuine Investors focus on businesses, not stocks.

Genuine Investing involves thinking like a business owner – every investment is a logical and careful purchase of a business, not simply a trade in a stock. Thinking like a business owner means only being interested in owning truly wonderful businesses; the sort of companies that sit within attractive markets, are steered by excellent and correctly incentivized management teams, and which possess a significant and enduring competitive advantage – so there can be confidence in consistent and growing cashflows well into the future. All these (and many more) features go into determining both the quality and also the value of any business.

And crucially, Genuine Investors understand that this underlying business value is often very different from a business’s stock price. The reason for this disparity is simple in principle, but most often overlooked. Business value (whether private or public) is derived from the future cash flows that can be produced for the owners over the long run. It is something that while subjective, can be estimated within a reasonable range and changes little over days, months, or quarters. Fundamentally, if you’re the owner of a business, your business is probably worth approximately the same today as it was six months ago.

On the other hand, stock prices change every second, often fluctuating as much as 50% in a quarter for no fundamental reason. Why the disparity? Because stock prices are driven by underlying business value PLUS many other factors. And those ‘other’ factors are typically short term in nature, impossible to predict, and often irrelevant to real underlying business value. Think of things like sentiment, asset flows, index inclusions, prices of other stocks, ‘style’ popularity, accounting rules, ratios, multiples, etc. There are hundreds of factors that drive stock prices up and down every day but have zero impact on the value of the underlying business.

For us as Genuine Investors, this disparity between business value and stock price presents a significant opportunity that can be exploited through a long-term mindset- because over the long run, stock price and business value always converge.

The reason is if short-term factors are depressing the price of a stock but the underlying business is grinding out consistent earnings growth, then eventually either the market will come to appreciate that underlying business value growth in the stock price, or someone will just step in and buy the whole business.

On the other side when it comes to overvaluation, stock prices may trade far in excess of business value based on exuberant sentiment, high peer valuations or asset flows into that ‘style’, but if over time the underlying business fundamentals aren’t keeping pace, those factors alone won’t be able to maintain the elevated share price indefinitely, or perhaps even company management will take advantage of the inflated stock price and issue more shares. Sooner or later, genuine business value always takes over.

Genuine Investors take advantage of this fact by focusing on business value and using stock price simply as an opportunity. And this approach to investing has a huge impact on the research process. Whereas most of the investment industry relies on reported accounting numbers, screening tools, ratios, and multiples to make their investment decisions, we as Genuine Investors know that accounting numbers are not only one small part of the overall process, but they are also often not telling us the true economic story of a business (see our recent series of articles on this subject). There are many far more important and more useful elements to consider: management teams, company culture, products and services, addressable market, competitive dynamics, regulations, etc.

And by using this approach, the investable universe shrinks considerably. After all, when you invest based only on owning wonderful companies, it quickly becomes obvious that there are entire industries which simply do not present attractive opportunities for investment despite what ratios and multiples might appear to be telling you. For example, there are many industries so heavily regulated that individual companies have little control over returns, there are many companies operating in declining industries, and many in markets so competitive that returns are miniscule.

Whereas passive (or ‘diversified’) investors will own many of these lower quality businesses, Genuine Investors are comfortable concentrating their capital in only the most attractive companies and industries available in the market. As a result, our portfolio doesn’t contain hundreds of stocks, nor does it contain exposure to many of the most common sectors or industries. Just because something is included in an arbitrarily constructed index like the S&P 500 doesn’t mean that we should own it.

But isn’t this concentration risky? To answer that question, we need to consider the impact that Genuine Investing has on portfolio risk management. Risk management is an incredibly important part of successful long-term investing, which is why it remains so startling to us that our industry does such an awful job of managing it.

The investment industry takes the view that the way to measure and control risk is through volatility – which is a measure of the historic variation of stock prices. Meaning the risk of a company is determined simply based on past movements in its share price. And what follows is that portfolios of fewer stocks are deemed riskier than portfolios of many stocks, as they are typically more volatile. We are comfortable saying that while that is the perceived industry wisdom – it is fundamentally wrong.

The industry uses volatility as a measure of risk because it is easy and impartial to calculate and can be integrated into sophisticated modelling, which provides mental security for investors. However, the underlying truth is that volatility is not risk. Volatility is backwards looking, it assumes a normal distribution, it is mathematically misleading, and it leads investors to make the wrong decisions at the wrong time (we have written more deeply on this topic in the past). But more fundamentally, the biggest problem is that volatility is solely focused on stock price, not business value.

Genuine Investors know that the real risk is underlying business value risk. Stock prices moving up and down (volatility) is not real risk. It is the underlying business value that drives long-term returns, and as such, it is the underlying business value that drives long-term risks.

So, instead of volatility, Genuine Investors focus on the risks to the underlying business, whether that is from competition, pricing pressure, regulation, industry shifts, consumer demands, etc. It is this focus on business risk that allows us to make the right decision when the rest of the market is panicking over increased volatility – as was the case during the Covid-19 sell off last year, you will recall that we spent little time worrying about price movements, our primary concern was whether business values would be impaired under these new circumstances.

Genuine Investing as an approach is not widely followed today because it is time consuming, difficult, requires considerable subjectivity and most importantly, it demands a long-term view in a world that is every more short-term focused. But as with most things, taking shortcuts tends not to pay off in the long run, and we are far more focused on creating and protecting long term wealth than short term fluctuations.

In closing, we would like to thank you all once again for your continued trust and loyalty in us as a team. We only have the freedom to implement such a measured and time-tested approach because of your continued support, and your fundamental long-term mindset as our clients.

Disclosures: This website is for informational purposes only and does not constitute an offer to provide advisory or other services by Globescan in any jurisdiction in which such offer would be unlawful under the securities laws of such jurisdiction. The information contained on this website should not be construed as financial or investment advice on any subject matter and statements contained herein are the opinions of Globescan and are not to be construed as guarantees, warranties or predictions of future events, portfolio allocations, portfolio results, investment returns, or other outcomes. Viewers of this website should not assume that all recommendations will be profitable, or that future investment and/or portfolio performance will be profitable or favorable. Globescan expressly disclaims all liability in respect to actions taken based on any or all of the information on this website.

There are links to third-party websites on the internet contained in this website. We provide these links because we believe these websites contain information that might be useful, interesting and or helpful to your professional activities. Globescan has no affiliation or agreement with any linked website. The fact that we provide links to these websites does not mean that we endorse the owner or operator of the respective website or any products or services offered through these sites. We cannot and do not review or endorse or approve the information in these websites, nor does Globescan warrant that a linked site will be free of computer viruses or other harmful code that can impact your computer or other web-access device. The linked sites are not under the control of Globescan, and we are not responsible for the contents of any linked site or any link contained in a linked site. By using this web site to search for or link to another site, you agree and understand that such use is at your own risk.