Market Update: The World is Ending (Again…)

For those of you who aren’t keeping score, the most recent daily returns of the stock market have been: -9%, 5%, -5%, -10%, 9%, and -12%. That -12%, which occurred yesterday, also happened to be the single worst day in US stock market history since October 19, 1987 (a title previously held by last Thursday). The move in the credit markets has been equally, if not more, dramatic. In short, there is currently a full-blown panic in the markets.

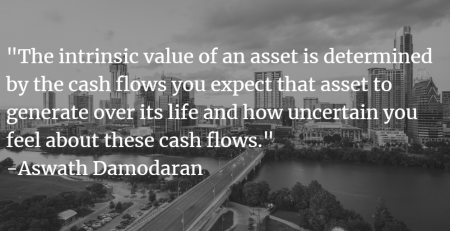

While it is true that we have comfortably outperformed the market/passive investing over this period, it is also true that our absolute returns have been negatively impacted by the selloff. We often pick on the market for being irrational in the short-term – market gyrations tend to dramatically disconnect from a company’s intrinsic value (i.e. the cash flows a company will produce over decades) and this is even more the case during a panic, catalyzed currently by all the uncertainty around Coronavirus.

What exactly is the uncertainty? Well, it is entirely possible that following the example in Italy, governments around the world begin to take the threat of this virus seriously – implementing social distancing measures along with massive fiscal, monetary and health care policies to stem the spread of the virus (we have started to see this already). This could then lead to the number of new infections dropping over the next few weeks (similar to what we have already seen in China and South Korea), followed by economies and markets rebounding vigorously as the worst is left behind us.

However, it is also possible that this doesn’t work – the spread of Coronavirus continues exponentially, hospitals are overwhelmed, tens of millions die, and the economy effectively shuts down for months to a year… followed, again, by economies and markets rebounding vigorously as the worst is left behind us.

Which outcome is more likely? No one knows, but along with the solace that both outcomes lead to the same place (although with differing durations of pain), we can tell you one thing for sure: Over the long run, 100% of all past crises have proven to be good buying opportunities.

Why is this the case? For one, we should recognize that humanity is really, really good at adapting to adversity (see numerous prior pandemics, world wars, famines, etc). Secondly, we should recognize that as stocks decline, even if they seem more dangerous in the short-run, they actually become more attractive over the long-run (this is basic math- you’re getting more for less). Lastly, and most importantly, no matter how bad things get during times of panic, the market will always overshoot to the downside, providing an opportunity for those with the temperament to take advantage of the situation.

Portfolio Example: What is an appropriate valuation response to a business slowdown?

A good example here is Mastercard – a company we have written about before. Mastercard is tremendously well defended by a network-based moat, as well as benefiting from the inexorable trend away from cash-based payments – a trend that is only accelerating along with the rise of e-commerce and an ever more connected world.

Mastercard’s stock price is down 31% over the last month. Now, giving Mr. Market some credit, it is true that a global shutdown of the economy (not an outcome set in stone) will affect transaction volumes negatively, and thus affect Mastercard’s earnings negatively.

But how do we know if a 31% correction is appropriate? The intrinsic value of a stock is measured by the present value of the cash flows that company will generate far into the future. In other words, in a perfect world, the stock price of any given company should represent what a business will earn not just next year, but also over the next twenty plus years. Think of it another way- if we were going to buy the whole of Mastercard and hold it as a personal private company, we’d want to know what it will generate for us in cash terms, so we can know what to pay for the business.

Now looking at the present situation, if we assume Coronavirus results in a huge global shutdown that rolls on for months, such that the earnings for Mastercard in 2020 are 50% lower than were expected at the beginning of the year (and there is no bounce back growth in subsequent periods to return us to the previous trend), then the per share valuation impact should be a decline of around 12%. Nowhere near the 31% fall we have seen so far.

Instead, what we are seeing play out in the market is what we always see – an overreaction to what is most recent. The market is selling down stocks as if companies will experience a huge slowdown this quarter, and for every upcoming quarter after that. In other words, overweighting the short-term and underweighting the long-term – the exact opposite of what prudent investors do. And it’s selling down almost all stocks regardless of their genuine underlying economic exposure to the virus or an economic slowdown. It is times like these that provide fantastic long- term opportunities for prudent investors.

This isn’t the first-time markets have crashed, and so long as markets are still made up of humans who have emotions (and this includes those humans who program algorithms), it won’t be the last. But take comfort in the fact that even with crashes like this the stock market remains the greatest long-term wealth compounding machine in the world.

Disclosures: This website is for informational purposes only and does not constitute an offer to provide advisory or other services by Globescan in any jurisdiction in which such offer would be unlawful under the securities laws of such jurisdiction. The information contained on this website should not be construed as financial or investment advice on any subject matter and statements contained herein are the opinions of Globescan and are not to be construed as guarantees, warranties or predictions of future events, portfolio allocations, portfolio results, investment returns, or other outcomes. Viewers of this website should not assume that all recommendations will be profitable, or that future investment and/or portfolio performance will be profitable or favorable. Globescan expressly disclaims all liability in respect to actions taken based on any or all of the information on this website.

There are links to third-party websites on the internet contained in this website. We provide these links because we believe these websites contain information that might be useful, interesting and or helpful to your professional activities. Globescan has no affiliation or agreement with any linked website. The fact that we provide links to these websites does not mean that we endorse the owner or operator of the respective website or any products or services offered through these sites. We cannot and do not review or endorse or approve the information in these websites, nor does Globescan warrant that a linked site will be free of computer viruses or other harmful code that can impact your computer or other web-access device. The linked sites are not under the control of Globescan, and we are not responsible for the contents of any linked site or any link contained in a linked site. By using this web site to search for or link to another site, you agree and understand that such use is at your own risk.