Second Quarter 2022 Update

Dear Partners,

Our performance in the first half of 2022 was disappointing in many respects. The S&P 500 had its worst start to the year in over 50 years. Bonds fared no better, with the 10-year treasury reaching its highest yield since 2011.

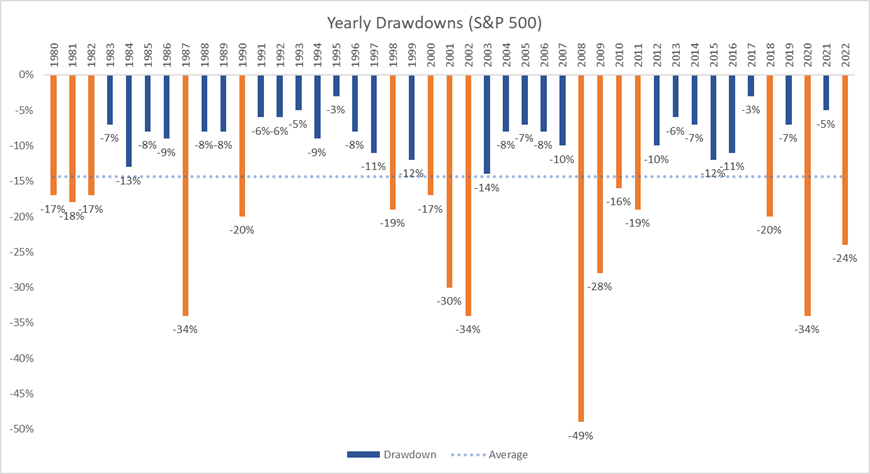

To put this into context, below is a chart of intra-year peak to trough equity market declines. So far, 2022 ranks as the 7th worst decline in over 40 years.

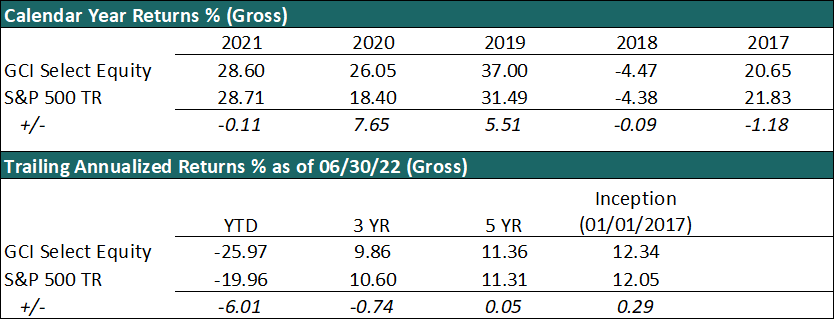

Against this backdrop, our GCI Select Equity composite trailed the overall market, ending the quarter down 25.97% YTD gross of fees.

For our long-term partners, periods of short-term stock price volatility like this year will come as little surprise. After all, we focus on providing long-run, risk-adjusted outperformance by investing in a concentrated portfolio of high-quality businesses at attractive prices. We do not focus on trying to beat the market over every reporting period, nor on trading in and out of whatever is currently in favor.

Will the Market Continue Falling?

The normal questions we get during any downturn are “are we at the bottom yet?” or “how much lower/ longer will this go?”. We continue to take the view that such questions are unanswerable – even if one could perfectly predict the thousands of variables that may drive short-term movements, they still wouldn’t be able to predict how the market would respond to those variables.

However, we can look to history for some guidance on where we stand today.

First off, the earnings growth of the S&P 500 has actually been positive this year – rising 6.7% as economies open up post-Covid and pent-up demand pushes up against supply chains that are still healing. Despite this fundamental growth, the multiples that investors are willing to pay for those earnings has fallen roughly 27% YTD. In other words, this drawdown has been led by a change in investor sentiment, not a change in underlying fundamentals – with the overall economy and businesses generally still in pretty good shape. In other words, this is not comparable to a 2008 meltdown situation, where the financial system itself was in structural danger.

Of course, this could change as inflation and a tightening Fed tip the economy into a recession. We may even already technically be in a recession (defined as two consecutive quarters of negative real GDP growth). But historically, even a recession doesn’t necessarily mean poor returns for investors.

Consider that since the end of the second world war we’ve had 12 recessions. In 11 of those 12 instances, the next two years of stock market returns were positive, with the median performance being ~25%. So, if we are in a recession right now, this would actually imply above average returns for stock market investors going forward. Note, markets almost always bottom before the economy and sentiment does.

For us, whether we are in a recession or not, and whether stocks bottom today or six months from now, is going to matter a lot less to our future performance than the cash flows our portfolio businesses are going to be able to produce for us years into the future.

Stock Price Volatility vs. Investment Risk

At times like this, risk becomes front of mind for investors. One of the single most important principles to understand when it comes to equity investing is that there is a difference between the real value of a business and the price of its stock. Following this logic, there is also a difference between stock price volatility and actual investment risk – in fact, stock price volatility is more akin to an investment opportunity, something that can provide us with the chance to acquire great businesses for less than they are worth.

On the other hand, real investment risk comes from the nature of certain kinds of businesses – with some businesses having far more or far less investment risk than others.

Take our portfolio holding GFL Environmental (GFL) as an example – a business that generates revenue by contractually collecting and disposing of waste. There isn’t much disruption risk in the fact that so long as humans exist, every single day thousands of tons of waste will be produced. To dispose of this waste, it is a safe bet that volumes will continue to go to the companies that have both hard to replace landfill assets, as well as route density advantages.

Compare this to say a pharmaceutical company where future revenues are determined by whether trials go well and whether drug approval is ultimately attained at the FDA. That’s not anything we can have any confidence in predicting next quarter, much less two decades from now. As a business, this carries far more business risk.

Or compare it to a young (and often exciting) company in a new and growing market that has not yet scaled enough to be standalone profitable and is therefore beholden to the capital markets for funding their operations. Since these new markets are so nascent (such as telehealth, electric vehicles, crypto-currencies, the metaverse, etc.), long-term unit economics are still unknown and a lot of risk lies not just in the future economics of the market, but in if a particular business will even survive to see that future.

Now when the share price of a low-risk, high-quality, profitable business gets cut in half (as many have this year) does that make investing in that business riskier? If the business itself has not been impaired, and yet we’re now able to pay less for it, then in fact it has become less risky.

Unfortunately, this logic is lost on many in our industry who see falling share prices and instead of getting excited, race to sell or downgrade their target prices. The fact that analysts think a real company is worth less just because its stock price has fallen makes no sense. And worse still, this effect also works in reverse – with businesses that have had significant real risk (SPACs, Unprofitable Growth, Innovation, etc.) often being ‘upgraded’ simply because their stock prices were going up.

On the bright side, it’s exactly this sort of broad-based institutional irrationality that provides such opportunity for genuine investors. As long as our industry remains so short-term orientated, there will always be opportunity for long-term investors such as ourselves. These are the periods when we get most excited.

With that in mind, let’s shift gears and discuss a new position we entered this quarter, Copart – a great example of the opportunities that can be found when markets fall, and great companies are sold off for no fundamental reason.

Copart, Inc.

Copart (CPRT) operates as part of a duopoly in the auto salvage auction market, along with their smaller peer, Insurance Auto Auctions (IAA).

In simple terms, the way the auto salvage market works is that if you total your car in an accident, your insurance company sends that car to one of Copart’s lots to be sold in a global online auction to dismantlers, dealers, etc. (matching local supply with global demand). Copart (usually) doesn’t take ownership of the car, they are just the middleman facilitating the logistics of the transaction, for which they take a commission.

Copart is a very high-quality business for several reasons. Firstly, the auto salvage business model is reliant on lots of land on which to store salvaged vehicles. That land needs to be close to wherever the vehicle crashed (reducing transport costs). Junkyard land is incredibly hard to come by, particularly in and around urban areas as zoning is very difficult to achieve since most people don’t want a 100-acre junkyard built anywhere near them.

Copart is the largest national owner of this rare industrial use land, with more than 250 yards and more than 10,500 acres – noting that they sometimes must wait 20 years for new land to open in a geography. This is a significant entry barrier, and similar the one that exists in landfills (GFL) or the cell towers (CCI, AMT). This relatively fixed cost asset base is not only a competitive advantage, but also allows Copart considerable earnings and cash flow leverage when they are able to put additional capacity through these assets. That excess cash flow then provides considerable reinvestment power, which supports even more land growth. This moat is incredibly strong and getting stronger over time.

Secondly, Copart’s model is classic two-sided online marketplace (like Facebook or Booking Holdings) a business model that is very hard to create, but once established often leads to some of the best economics in the world with incredible barriers to entry. One of the beautiful things about these networks is that customer acquisition costs decline as these networks grow, leading to incredible incremental economics. With Copart, insurers want to send their salvaged cars to where the most bidders are to ensure a good sales price, and bidders want to come to where the largest selection of salvaged cars are.

Thirdly, Copart benefits from a non-cyclical and stable end market – simply because people continue to crash cars in good times and bad times. The overall crash rates per year are in fact mostly dependent on the physical stock of cars on the road and miles driven, both of which tend to increase fairly steadily each year.

Finally, Copart is a wonderful example of strong corporate culture, management discipline, and alignment with shareholders. The original founder Willis Johnson now serves as Chairman, with his son in law Jay Adair as CEO. Before anyone screams ‘nepotism’ – Jay worked at Copart long before becoming Johnson’s son in law. As CEO, Jay is arguably underpaid compared to his counterparts in salary terms, because he instead chooses to receive his compensation predominantly in stock.

Indeed, there is significant stock ownership throughout the board – an excellent example of shareholder alignment. In addition, this management team have repeatedly displayed their caliber and ability throughout their tenure, such as standing publicly apart from their competition in supporting customers by refusing to take advantage of natural disasters by putting through aggressive price hikes. The management team have also consistently been great capital allocators, particularly in regard to stock buybacks where they have been both highly selective, and at times aggressive.

Copart isn’t a company where management blindly buys back stock consistently, regardless of price or potential returns (unlike other less rational management teams), instead management will only conduct buybacks when the returns on those buybacks exceed their other investment opportunities – exactly as buybacks should be.

Going forward, the incremental value creation for us as investors here will depend on a few key variables:

- Total loss rates – this is simply the number of cars that get salvaged versus those that are sent to a repair shop. Total loss rates have been trending up from around 4% in the 1980s to about 20% today. There are some secular trends driving this steady increase. For one, Americans are holding onto their vehicles longer with the average age of vehicles on the road at record highs – with older vehicles more likely to be salvaged than repaired when they get into an accident. Another trend is that cars are getting more expensive to repair as their complexity increases. Cars today have sensors, cameras, and various expensive electronics all over them, meaning even minor damages can now be simply too costly to repair.

- Average Selling Price – The largest source of revenue for Copart is the commission they take on the sales price of vehicles in its auctions. In the past, a salvaged car might have just been worth the cost of the metal it could be broken down into. Today, with more and more cars being deemed salvage due to the excessive costs of repairing, much higher value cars with just dents and minor cosmetic issues are flowing through Copart’s auctions. Furthermore, as Copart has expanded their auctions internationally they have increased the liquidity of their auctions, leading to higher bids and thus higher revenues.

We believe there remains a long runway here for reinvestment into salvage land at c30% returns on capital. Copart should be able to drive c5% volume growth due to total loss rates increasing and another c5% on the pricing front. And add to that the significant opportunity to continue their international expansion (UK, Ireland, Germany, Dubai, etc.), as well as operating margin leverage from a reasonably fixed cost base, and we can comfortably see mid-double-digit earnings growth over the medium term, with our downside likely supported by aggressive buybacks at more accretive prices.

Thank You

As always, we would like to take this opportunity to thank you, our partners for your continued trust in us and our approach. After all, the success of any investment strategy depends on a mutual understanding between us as the manager, and you as our investors and partners on what our ultimate goal is and how we intend to achieve it.

Please feel free to reach out to us with any questions you may have, or if you would like to discuss any of this further.

Kind regards,

Guy Davis, David Shahrestani

Disclosures: This website is for informational purposes only and does not constitute an offer to provide advisory or other services by GCI Investors in any jurisdiction in which such offer would be unlawful under the securities laws of such jurisdiction. The information contained on this website should not be construed as financial or investment advice on any subject matter and statements contained herein are the opinions of GCI Investors and are not to be construed as guarantees, warranties or predictions of future events, portfolio allocations, portfolio results, investment returns, or other outcomes. Viewers of this website should not assume that all recommendations will be profitable, or that future investment and/or portfolio performance will be profitable or favorable. GCI Investors expressly disclaims all liability in respect to actions taken based on any or all of the information on this website.

There are links to third-party websites on the internet contained in this website. We provide these links because we believe these websites contain information that might be useful, interesting and or helpful to your professional activities. GCI Investors has no affiliation or agreement with any linked website. The fact that we provide links to these websites does not mean that we endorse the owner or operator of the respective website or any products or services offered through these sites. We cannot and do not review or endorse or approve the information in these websites, nor does GCI Investors warrant that a linked site will be free of computer viruses or other harmful code that can impact your computer or other web-access device. The linked sites are not under the control of GCI Investors, and we are not responsible for the contents of any linked site or any link contained in a linked site. By using this web site to search for or link to another site, you agree and understand that such use is at your own risk.

All references and views offered, including but not limited to stocks, companies, investments, investment styles, market returns, expectations, forecasts or estimates and any other area of investing are the opinion of the manager and should not be taken as facts, projections or guarantees. All such opinions are subject to change are do not constitute a recommendation or solicitation to buy or sell a particular security.