Third Quarter 2022 Update

Dear Partners,

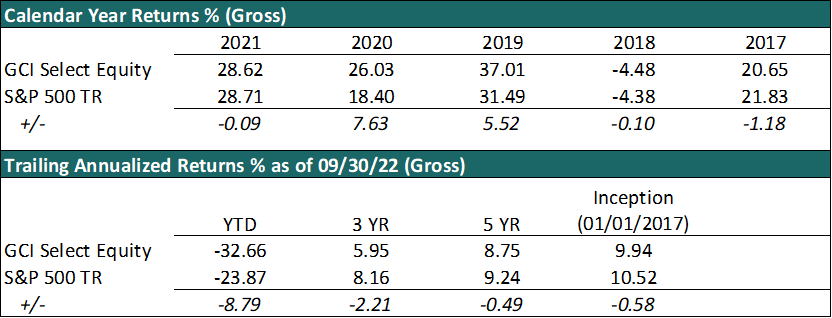

Our performance in the third quarter of 2022 was disappointing. Our GCI Select Equity composite ended the quarter down 32.66% YTD gross of fees, trailing the broader market. This is a significant drawdown in isolation, but also not entirely unsurprising to have some weakness after almost a decade of very strong returns.

As far as current market conditions, it is easy to get caught up in the magnitude of the current fall and the day-to-day negative news flow – whether that be inflation, the war in Ukraine, or the continued policy blunders in the UK.

But as long-term investors we should always remember that crises like this are nothing new – in fact, history is littered with recessions, depressions, inflation, pandemics, wars, elections, etc. and yet global markets continue to compound through it all.

Markets may continue to go lower in the short term from these levels, but for anyone who can take a longer-term view, this recent fall should be viewed as an opportunity – after all, in three years’ time it is unlikely anyone will remember whether the monthly inflation print was 8.3% or 8.1%, while today the media often seems to imply that’s all that matters.

As you know, GCI was founded on the principle that investing in high-quality companies at attractive prices is the most durable and consistent way to achieve long-run, risk-adjusted returns. While we aim to outperform the market over the long run, we do not expect to outperform every single year.

Consider that our equity portfolio today consists of just 21 companies, so it bears little resemblance to a broad index such as the S&P 500. As you know, we are highly selective when it comes to the companies we own. There is a very high threshold of not only underlying business quality, but also valuation. While this approach has for decades produced significantly market-beating returns, there are always going to be short term periods of weakness.

Always remember that stock market prices can and do move independently of underlying business value. We can often see real business value compounding upwards even while share prices may be falling. For many high-quality companies in the market, that’s exactly the situation we find ourselves in today.

When significant declines such as this occur, the best thing for any investor to do is look closely at the underlying assets they hold – are these companies continuing to grow earnings, and therefore real business value? If so, then we can be confident continuing to hold. In fact, we may even choose to add to some positions where stock prices have come down significantly while business value may have increased. It is often during these difficult times that the best future returns can be locked in.

Not only do times like this create opportunities for us to add additional value at the portfolio level, but they can also create opportunities for our portfolio companies themselves to do the same at the underlying company level.

While it may not always be immediately apparent, most of the companies we own are run by shrewd management teams that have positioned their firms to take advantage of this market turbulence either through market share gains as less robust competitors falter, opportunistic acquisitions, or through the repurchasing of their own stock. We expect many of our portfolio companies to not only survive this current market drawdown, but to come out of it stronger than they would have been otherwise.

By way of a brief example of how we are taking advantage of the recent downturns, below is an introduction to a new position for us, Texas Instruments, as well as some commentary on two of our worst performing positions over the quarter, CarMax and Ocado.

New Position: Texas Instruments Inc. (TXN)

TXN is a business that has been on our watchlist for years, only recently pulling back to a level where we were comfortable owning it.

Very high level – TXN designs, manufactures, and sells analog semiconductors to electronics designers and manufacturers worldwide. For example, when your thermostat tells you what temperature it is in your house, or when your car tells you your tire pressures, that is possible because of analog chips. Analog chips can interpret continuous variables like the above examples, while digital chips can only interpret binary variables like 1 or 0.

A good model for thinking about TXN is the “small thing into big thing” keystone product model where the value a business provides to its customers is extremely high relative to the price being charged.

The analog chips that TXN sells might cost less than a dollar and then go into product platforms that might cost 10s of thousands of dollars, like a car. In other words, these are often mission critical components with very high-performance requirements that are designed into product platforms that may last decades. As such switching costs are high and market share in the industry is very stable, only really shifting through M&A.

You have probably heard us talk about how we largely avoid the semiconductor industry because of both cyclicality fears, as well as the fear of technological disruption. The players in the space that operate at the precipice of technological innovation (Intel, AMD, Nvidia, Samsung, Qualcomm, etc.) are continually leapfrogging or falling behind each other due to their pace of innovation (or lack thereof).

This is not the case with TXN and the analog semiconductor industry. Analog products don’t really become obsolete in any given year and while cyclicality is still an issue, inventory will not need to be written down as in other industries.

Consider that the two most important end markets for TXN are industrial and automotive – both of which offer secular growth going forward. Factories are being equipped with ever more sensors while automotive vehicles are expected to double their semiconductor content over the next decade as the shift to electric vehicles continues. When a TXN chip is awarded a place on any of these platforms, it is likely that place will remain relevant many years into the future, much longer than the average market participant is even considering.

What we end up with is a very stable business with little market share shifts and secular tailwinds behind it that produces massive cash flows. The management team here has proven to be excellent capital allocators in the past, a benefit we expect will continue going forward.

Management takes a logical (and sadly rare) approach to share buybacks – increasing them when their stock price is falling and pulling back when their share price is high. Just this past month they announced a further $15B buyback on top of the $8.2B they already had outstanding. This $23B repurchase program represents roughly 16% of their market capitalization today.

The reason we believe we are getting the opportunity to own this great business at what we would call a depressed valuation is likely because the company is going through a capex cycle at the same time that cyclical fears in their end markets are starting to build.

Free Cash Flow will likely remain depressed for the next few years as new semiconductor fabs are built to support more revenue growth. But by our math, the returns on these new fabs are likely to be in the 30% range. The market hates companies where they are spending money today, but the reward for that won’t come until a few years down the line. Lucky for us, we have no issue with this setup.

We expect topline to grow 7%-8% through cycle, with margin expansion and share buybacks, FCF should compound at a high single/low double-digit rate for many decades to come. At today’s depressed valuation, we expect a mid-teens IRR on our investment for what we believe is one of the highest quality businesses in the market.

And we take further comfort in that if the market continues to sell off, TXN is in a great position to both buyback a large portion of the market capitalization as well as pursue opportunistic M&A.

Performance Detractor: CarMax, Inc. (KMX)

One of our largest detractors in the quarter, KMX, was down 20% in a single day due to an earnings report that suggested same-store-sales deteriorated at a mid-teens rate year on year into August and September. Management blamed macroeconomic factors such as “vehicle affordability challenges that stem from widespread inflationary pressures, as well as climbing interest rates and lower consumer confidence.” We used the share price weakness to add to our holdings of KMX.

As a reminder, KMX is our country’s largest seller of used cars. Last year, as the production of new cars slowed due to supply chain issues, there was a large surge in demand for used cars, leading to increasing prices and sales for KMX. This year as those high prices have acted as a speed bump on demand, it is very likely that KMX will sell fewer cars than they did in the prior year, a setup which the market’s short-term bias never likes.

But taking a longer-term view, KMX has leveraged its position of strength to use this recent market volatility to capture more market share in what is ultimately a scale-based business (brand marketing, inventory sourcing, fulfillment proximity, technology spend, inventory turnover). We believe that this strategy will lead to an even stronger franchise coming out of this down cycle.

Today, the stock trades for under 12x 2019 EPS (fiscal year ending February 2020). Consider that back then, KMX had roughly 3.5% market share, 216 used car stores, and a largely offline business. Today, KMX has roughly 4.0% market share, 230 used car stores, and a fully omnichannel business, allowing customers to buy online, offline, or any combination thereof, which we believe should be conducive to higher through cycle returns as the costs of this model are optimized over time.

With only 4% market share of a massive ~$750B market, we believe there is still a long runway of moat-protected low-double-digit EPS growth to be had here, and at a valuation that adds further upside to our returns as shareholders. We are pleased to add to our holdings of this leading franchise at a steep valuation discount to both the market and its historical average.

Performance Detractor: Ocado Group Plc (OCDDY)

Ocado stock is down ~60% YTD. We believe that’s an overreaction, and that it presents a significant buying opportunity today. Here are the facts:

- Regardless of any short term COVID/ re-opening impacts, each year more people want groceries delivered than the prior year. This is a consistent shift and will continue for many years to come.

- Despite numerous entrants, Ocado still sits head and shoulders above any competitor when it comes to managing grocery delivery profitably. Almost none of the competition are profitable, and certainly none can offer the full breadth of services that Ocado can. This remains a one-horse race.

Ocado has two businesses today: a UK online-only supermarket and an international licensing business of their end-to-end delivery technology to other retailers. While the UK business has been operating for many years, the international business is still in its infancy and has yet to produce any meaningful revenues. Put together, the company continues to be loss-making as they are investing heavily in building international capacity.

For the last 6-9 months, Ocado’s share movement has been dominated by newsflow around just the UK business which represents most of the earnings today, but in the future will be a small portion of the overall value of the business as the international licenses are set to generate significant revenue and earnings growth in the next few years.

This is creating a significant opportunity for investors today – based only on the contracts that have already been signed, Ocado is going to generate annual revenue of ~£1bn from its international business, likely as soon as 2026 based on their current build rate. That revenue is also likely to come with around 50% EBITDA margins, so we’re looking at ~£500m of earnings or around 5x the size of the current UK business.

That is purely from the contracts already signed and in place, assuming no further growth. But in reality, it’s likely that the existing contracts continue to grow in scale as they have done already (more distribution centers per customer), as well as them adding new customers.

Right now, Ocado is trading at a market cap of less than £4bn, for a business that we believe is likely to be generating more than that in annual sales in just a few years’ time. And notably, the share price today is now back to the level it was at before any of the international business even existed. Having raised equity in recent years, the company sits with almost £2bn in liquidity, which should be more than enough to see them through to cashflow breakeven.

We see this as a great example of classic market short-termism and lack of genuine business analysis. A small number of temporary issues that hurt the current UK business is all the media and the market have focused on, while in the background the company continues to execute on the international opportunity, which will be the driver of our returns going forward.

Thank you

As always, we would like to take this opportunity to thank you, our partners for your continued trust in us and our approach. After all, the success of any investment strategy depends on a mutual understanding between us as the manager, and you as our investors and partners on what our ultimate goal is and how we intend to achieve it.

Please feel free to reach out to us with any questions you may have, or if you would like to discuss any of this further.

Kind regards,

Guy Davis, CFA, David Shahrestani, CFA

Disclosures: This website is for informational purposes only and does not constitute an offer to provide advisory or other services by GCI Investors in any jurisdiction in which such offer would be unlawful under the securities laws of such jurisdiction. The information contained on this website should not be construed as financial or investment advice on any subject matter and statements contained herein are the opinions of GCI Investors and are not to be construed as guarantees, warranties or predictions of future events, portfolio allocations, portfolio results, investment returns, or other outcomes. Viewers of this website should not assume that all recommendations will be profitable, or that future investment and/or portfolio performance will be profitable or favorable. GCI Investors expressly disclaims all liability in respect to actions taken based on any or all of the information on this website.

There are links to third-party websites on the internet contained in this website. We provide these links because we believe these websites contain information that might be useful, interesting and or helpful to your professional activities. GCI Investors has no affiliation or agreement with any linked website. The fact that we provide links to these websites does not mean that we endorse the owner or operator of the respective website or any products or services offered through these sites. We cannot and do not review or endorse or approve the information in these websites, nor does GCI Investors warrant that a linked site will be free of computer viruses or other harmful code that can impact your computer or other web-access device. The linked sites are not under the control of GCI Investors, and we are not responsible for the contents of any linked site or any link contained in a linked site. By using this web site to search for or link to another site, you agree and understand that such use is at your own risk.

All references and views offered, including but not limited to stocks, companies, investments, investment styles, market returns, expectations, forecasts or estimates and any other area of investing are the opinion of the manager and should not be taken as facts, projections or guarantees. All such opinions are subject to change are do not constitute a recommendation or solicitation to buy or sell a particular security.