Fourth Quarter and Full Year 2020 Update

Dear Clients,

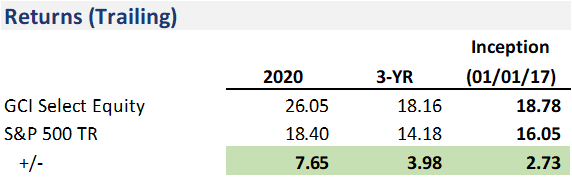

We are pleased to report that 2020 was another positive year for performance in both absolute and relative terms.

As you know, Globescan Capital was founded on the principle that investing in high-quality companies at attractive prices is the most consistent way to achieve long-run, risk-adjusted returns. As such we do not overly concern ourselves with short-term market swings driven by ever-changing sentiment shifts or short-term news flow. This rational and disciplined approach benefited us greatly throughout the year.

As we enter 2021 we would like to take this opportunity to thank you, our clients, for your continued loyalty and trust. We are very fortunate to have the client base and partners that we do as it is the stability and shared vision of you as our clients that provides us with the foundation to be able to deliver such good performance. The importance of this is seen most during times of stress – during the market panic of Q1 2020, we are proud to say that while asset managers around us were seeing redemptions; we saw continued positive inflows throughout the period. This was a trend that continued throughout 2020.

2020, Covid-19, and The Folly of Short-Term Predictions

The story of 2020 was dominated by the world’s response to the Covid-19 pandemic, which continues to create serious human hardship and suffering, disrupting thousands of lives. Our job as investors is to understand the implications of Covid-19 on the businesses we hold, as well as to study the lessons we can learn from this period that will make us better investors in the future.

Looking back at our commentary during the early days of the crisis highlights our consistent approach to investing, even in times of market panic:

- February 27: “It is human nature to overreact to short-term crises, and the market is more guilty of this than anyone. Our job is to take a step back, think long-term, and instead ask what this move means overall, and what investment opportunities might be being created.”

- March 17: “Which outcome is more likely? No one knows, but along with the solace that both outcomes lead to the same place (although with differing durations of pain), we can tell you one thing for sure: Over the long run, 100% of all past crises have proven to be good buying opportunities.”

- March 24: “While it is true that Covid-19 will be a net negative impact on economic activity in the short run, it is also true that at times like these market prices aren’t driven by the economy – rather, they are driven by a combination of emotion and a search for liquidity as forced selling overwhelms any rational buying demand.”

As always, we never made any short-term predictions about what would happen with either the virus or with the markets – we have little ability to forecast either reliably. Instead, we focused less on what was happening in the day to day and more on the implications for our portfolio holdings over year to year. This is what long-term investing is all about – arbitraging the difference between short-term sentiment shifts and long-term business fundamentals.

Unfortunately, many market participants do not take such a pragmatic approach to investing. Instead in the face of a looming crisis the inherent need to feel like one is “doing something” often overrides all common sense. Market pundits and sell-side analysts see that things are bad today and then forecast that things will be bad forever.

Passive investors, with no underlying fundamental basis for why they hold their positions, listen to the pundits, and sell at the worst possible time. Additionally, professional investors with poorly designed risk tools see that markets have become more “volatile” and sell at the same time to lower their “risk”.

This is because when the market crashed 30% in a matter of weeks, most wealth managers were required to sell stocks because their risk tools and portfolio management software instructed them to. The reasoning is simple: equities fell, leading to an increase in volatility. Increased volatility is translated as more risk for these portfolio management tools, which means that they must sell more of their positions to reduce that risk, which leads to even further volatility… and so on and so on. All of this creates a powerful negative reinforcement cycle- driving the markets lower.

Let us be clear, even if we had a crystal ball that told us exactly how Covid-19 would play out this past year, it would not have told us how the market would react. Instead, our best map for navigating any crisis will always be an understanding of the underlying fundamentals of the companies we invest in and the drivers of their future.

We know that stocks represent real business ownership, they are not simply numbers on a screen, and risk is not simply the movement of those numbers on a screen. We also know that if an asset becomes cheaper, it is (all else equal) in fact less risky, rather than more risky. We are therefore in the ideal position to sit calmly while those around us are panicking, to rationally assess the actual impact on real business value, and then act accordingly. It is only this that will give us the confidence to step in and calmly buy more shares when the rest of the world is hitting the sell button. This is the most important investment lesson to take away from the year. The short-term prediction game that many rely on is nothing more than folly.

Trading Activity in 2020

Our portfolio activity in 2020 was somewhat unusual, because the market environment in 2020 was somewhat unusual. As we mentioned, our fundamental analysis positions us to take advantage of severe market volatility. For example, when the first global lockdowns began in early 2020, we immediately started in-depth stress testing of our portfolio companies. There were three in particular that we expected would be most negatively impacted by a global shutdown: Booking Holdings, Wyndham Hotels, and CarMax. Our question was simple, could these companies survive months to years without any revenue?

We focused on solvency concerns; how was their balance sheet structured, what liquidity did they have available, what liquidity could they access, how much of their cost base was variable and could be cut, how much of the fixed costs could be shifted to variable costs, etc. We spoke with the companies themselves, we looked at competitors, we looked to other countries in differing stages of lockdown, and we tried to build an overall picture of how long these companies could survive in a worst-case scenario. In all cases, our analysis pointed to security for well more than a year, providing a significant margin of safety.

At the time we were doing this analysis, the world was already in lockdown and we had no way of knowing if lockdowns would last 3 months or 30 months. But what we did know was that even in full lockdown, revenue for our businesses hadn’t fallen to zero.

Take Wyndham Hotels as an example: even in the absolute depths of the crisis, occupancy rates did not fall below 30%. Similar was true for Booking Holdings and CarMax. As a result, we were confident that there was very little solvency concern with these companies. Despite this, some of the share prices had fallen by more than 75%. Such a reaction was in our view excessive and not representative of the real decline in business value.

As a result, in March we did something that we do very rarely – we made several substantial portfolio shifts in a short space of time. We raised cash from names that had held up very well (UPS, Equinix, and American Tower) and we began buying more of Booking, Wyndham, and CarMax. It was a direct result of our deep knowledge of these businesses and our approach of taking a fundamental rational approach to looking at the underlying businesses that gave us the confidence to be able to make these purchases when those around us in the market were panic selling.

While we expected that we would generate good returns from this shift, we did not expect they would come so quickly. In the following six weeks from our purchases, we experienced a monumental market rally, which was even greater in those names we had been adding to. By way of example, Wyndham Hotels stock price tripled in a matter of weeks. Such was the speed of the recovery that our outsized expected returns compressed, leading us to then reverse the portfolio shift in mid-May; we simply put the portfolio back to how it had been at the beginning of the year once these extreme valuation anomalies had corrected.

This move proved to be very beneficial for our portfolio, but such changes do also make us look far more short term focused than we are in reality. As a result, our headline 2020 portfolio turnover number will be much higher than normal. Over the long run, you should continue to expect our strategy to be low turnover under normal conditions, but will also not hesitate to act quickly when unusual opportunities emerge, as we did this year.

Where We Stand Today

We started 2020 by writing in our 4Q19 letter:

It is important that we are all on the same page in that, although 2019 was a fantastic year for our investments, no single year of performance will determine long-run compounded returns. Consider a few points:

- In 2019, the S&P 500 returned 31%

- On average, US equities have historically delivered 8-9% per year

- On average, each year there is be a 14% peak to trough sell-off

This isn’t to say that there will be a 14% correction soon (though statistically, it is likely at some point during 2020), or that we are due for a bear market, or that we can bank on an 8-9% return every year for the foreseeable future. It is to say that in any given year the stock market will go up and down and in the short term it is largely unpredictable and irrelevant to our strategy, outside of the fact that it creates opportunities for us.

Almost the exact same could be said for 2020, and while the 2020 S&P 500 performance did not match the 31% from 2019, it still came in at a very healthy 18.4% – during one of the worst pandemics in nearly a century. So where do we stand today? Here are a few points to consider:

- Over the last ten years, the S&P 500 has compounded at an annual rate of 13.8%, well above the long-term historical average of 8-9% per year.

- Over the same period, the yield on the 10-yr Treasury has fallen at an annual rate of 12.7%, providing a tailwind for stock prices.

- Interest rates remain at historic lows, even negative in many regions, but if this were to change that tailwind would turn into a headwind.

- Tesla ended the year +740%.

- Bitcoin ended the year +302%.

- More IPOs have doubled in their debuts this year than any year since the 2000 tech bubble.

- 2020 saw 234% more IPOs than an average year, and there is little evidence of this slowing into 2021.

- More money was raised for SPACs (Special Purpose Acquisition Companies) during 2020 than in the last ten years combined.

At present, there are certainly signs of froth in parts of the market. But despite this, there are also many stocks attractively priced; opportunities that are not available to passive investors as many indices are now dominated by big (and often expensive) technology companies.

At times like this when there are some clear areas of overvaluation in the market, it is useful to revisit the concept of investing versus speculating. When you invest, you allocate capital thoughtfully and carefully in specific assets that you think will generate a positive real return over your holding period. This involves analyzing the fundamentals of the company in question and the future cash flows we can expect to receive as investors.

When you speculate or ‘trade’ you are buying an asset in the simple hope that someone else will pay more for that same asset in the future. Your odds of a good outcome rely on how well you can predict specific outcomes, events, or the behavior of other (often irrational) individuals. Those who make these ‘predictions’ often base them on past patterns which themselves are altered by the act of speculation- like trying to hit a target when the simple act of aiming moves the target.

We would argue that a lot of the excess we are seeing in the market today in specific assets (Tesla and Bitcoin are two obvious examples) is the result of speculation run amok. Humans naturally like to gamble and wherever the possibility of rapid and massive gains can be found, speculators will be there to inflate huge bubbles, which are then often followed by huge crashes in a near-endless cycle.

In our minds, this is a disappointing waste of humanity’s energy and resources, much like any casino. After all, shouldn’t we encourage the building of productive assets that will be a net positive for society going forward, and discourage the hoarding of purely speculative assets? Would the world be better off if Steve Jobs, or Bill Gates put their early wealth into a speculative asset like Bitcoin and sat on it for half a century rather than building the businesses the modern world has come to rely on?

The truth is that there will always be something returning 100x. There will always be someone winning the lotto. The hardest part of any cycle is when everyone else seems like they are getting rich. This is when we need to take a step back and compare the narrative to reality. As Buffett likes to say, “The less prudence with which others conduct their affairs, the greater the prudence with which we should conduct our own.”

Before we move on, it is worth again remembering that due to the concentrated and long-term focused nature of our portfolio, significant performance deviation from stock indices should continue to be expected. Over the medium and long term, we expect this to continue to be positive, as it has been in recent years (otherwise you may as well just buy the index) – but there will be, without a doubt, times when our portfolio is behind that of the broader market in the short term.

Such periods are to be expected, are not any cause for concern and crucially, will not cause us to alter our strategy. Our approach consistently generates attractive risk-adjusted returns over the long term and we have no desire to ‘chase’ market trends or fads in the short term. We will continue to approach investing with the same discipline we have always done.

Portfolio Review

As we move into 2021, we are very confident in our portfolio of companies despite the froth in some areas of the market. We are confident that we are holding a reasonably small group of very high- quality companies that will be able to consistently compound earnings for us. And based on our assessment of business value, we still do not believe the market is fully recognizing the underlying intrinsic value of these businesses.

The best way to express our confidence in the portfolio is through the companies themselves. What follows are short summaries for our top 10 equity holdings which make up more than half of our equity book:

FACEBOOK, INC.

Facebook is without a doubt one of the most influential companies of the last decade. They have created the largest social network the world has ever seen, which is also probably the most detailed network the world has ever seen as far as their capacity for data collection. Never before has one organization known so much about so many people. Whether you think that is a good thing or a bad thing, it is clear that this network is incredibly valuable – even if conceptually it is very hard to ascribe an actual dollar value to it.

Despite the incredible breadth, depth, and value of this network, Facebook shares continued to trade well below our estimate of intrinsic value in 2020 – most likely due to concerns that the company would be regulated, split up, or otherwise restricted from being able to monetize their data.

Even considering these very real risks, we find Facebook to be an attractive value on a risk-adjusted basis. As we see it, investors today are getting one of the world’s preeminent online advertising platforms for arguably fair value, and then on top of that, we get a whole host of upside options for effectively free: Facebook Shopping, Facebook Payments, Oculus, WhatsApp monetization, Reels monetization… the list goes on. Upside opportunities like these are vast across their platform.

Of course, we would prefer that Facebook was not in the crosshairs of regulators (as it has been for much of the last few years), but we must understand that it is precisely that negative sentiment that has allowed us to build a position at attractive prices in the first place.

AIR PRODUCTS AND CHEMICALS, INC.

Air Products build, own, and operate large-scale gasification plants that produce gasses (oxygen, nitrogen, hydrogen, etc.) for use in a variety of different end markets. Substantial amounts of gas are required in a wide (and increasing) variety of industrial processes: steel production, oil refining, food processing, and medical applications, as well as huge nascent future trends such as hydrogen mobility. When it comes to the attractiveness of an industry for investment, industrial gasses are one of the better ones for sure.

For many large-scale industrial applications, APD will build a multi-billion-dollar gasification plant on-site at a customer’s production site. This is a tremendous value proposition: the customer shares the cost of the build, and then commits to a minimum volume on 15-20 yr. ‘take or pay’ contracts. Air Products can therefore make substantial capital investments with certainty over their long-term returns. Such a proposition is rare in the investing world. These large-scale plants make up over half of APD’s earnings, with another third coming from ‘bulk’ gas and liquid- this is truckload sizing delivery rather than on-site plants, this area also comes with reasonably good contract terms- typically 3-5 years.

Given their long-term contracts and certainty over returns, the track record of APD as an investment is understandably impressive. The company’s incredibly stable returns throughout economic cycles have enabled them to increase their dividend every year for the last 37 years.

The main differentiator for APD today is their huge capacity for investment in the future- they sit with a very conservative balance sheet, providing them with around $17bn available to invest over the next 2 years. With the consistent returns and strict hurdle rates that APD applies to any development, this is a considerable amount of additional cash flow that the company can create for the future, over and above the existing business.

The shares were weak during late 2020 as there was concern around a large project (Jazan) being delayed or potentially halted altogether. We have been acquiring more shares during this weakness- as whatever happens with the Jazan project, APD has a huge number of other potential opportunities to invest their cash at very attractive rates. Any short-term delay is a concern to the quarterly focused investors, but to long term holders, like us, it merely provides us with an even more attractive return profile.

MICROSOFT CORPORATION

Microsoft is probably best known for its Windows operating system, though today Windows is a small portion of Microsoft’s business, now massively overshadowed by their Cloud (Azure) and Productivity Software suite of services (Office).

In the cloud, Azure is well-positioned to gain share in a fast-growing, massive market opportunity where they are a more natural partner for enterprise customers compared to the current market leader, Amazon’s AWS. While scale is key in this market, Azure stands in the unique position of being the only cloud company who participates at every single layer of the cloud ‘stack’ from software all the way down to physical hardware, and every stage in between. Outside of the cloud, Office remains one of the best businesses of all time on a stand-alone basis and looks even better when we realize Microsoft can leverage their massive installed base as a touchpoint for customer acquisition in Azure.

And that customer acquisition accelerated significantly during 2020, as Covid-19 stay at home orders forced corporations around the country to reassess their cloud-based infrastructure- or more often lack thereof. It is now entirely possible that Microsoft could equal AWS in market share terms within just five years.

Putting everything together, and we are looking at a $1T mission-critical company that is growing faster than many smaller companies and doing so with tremendous operating leverage. While Microsoft may look expensive relative to its past, their market opportunity and growth rates far outpace historical comps, and the company should be able to deliver at least mid-to-high teens EPS growth going forward with upside from deploying their significant cash balance.

MASTERCARD INCORPORATED

Mastercard is a tollbooth business – collecting a fee on electronic payments regardless of whether those payments are credit, debit, online, mobile, etc. Their position in the market is extremely well protected due to a very difficult chicken and egg problem that would-be competitors would need to solve – issuers want to issue cards that consumers want to use, consumers want to use cards that merchants accept, and merchants want to accept cards that issuers issue. This creates a powerful network effect as the more of each party on the network; the more convenience, the more data, the more secure, the better the overall network is for everyone, which explains why only a handful of networks have come to dominate the market over time.

Mastercard sold off with everything else in 2020 as it became apparent that global payment volumes (especially cross-border volumes) would be depressed in a Covid-19 locked-down world. But did anything fundamentally change with the Mastercard story 3, 5, 10-years out? No, and as such this was a great opportunity to add to our position. By way of a guide, even if you assumed Mastercard’s earnings would drop by 50% during 2020 (highly unlikely given the boom in ecommerce), the valuation impact should only have been in the region of 15%. As always, the market over-reacted in the short term- marking the shares down over 30% in March.

Going forward, Mastercard’s earnings growth will be driven by the continued secular trend away from cash-based payments – a trend magnified by the inexorable shift towards e-commerce and the increasing ease in which Merchants can access Mastercard’s network (mobile payments, browser payments, smart speaker payments, IoT payments, etc). We believe that the market is failing to price in the likely step up in growth these trends will bring Mastercard.

CHARLES SCHWAB CORPORATION

We were fortunate to start a position in Charles Schwab during 2020 right before a significant rally in its share price. (Bear in mind any very short- term moves are more luck than judgment). We have long respected the Charles Schwab business fundamentally, particularly the focus on treating their customers so well that it hurts their short-term financials but creates enormous long-term value.

Consider that late last year Charles Schwab made the decision to completely end the business that birthed them, by taking trading commissions to zero. This was not a move from a position of weakness due to price competition, but from a position of strength due to their ability to share their scale economics with customers. They had gradually built the business around them such that they were able to remove commissions without a significant impact to their bottom line (the same could not be said of competitors such as TD Ameritrade). Indeed, such was the impact on the share price of TD Ameritrade that Charles Schwab stepped in to buy them and have set themselves up with the potential for many years of positive returns as they gradually integrate the TD business into their own.

The overall approach of Schwab is similar to the Costco model – a retailer that doesn’t make any money retailing; instead passing their scale economics on to the customer in exchange for profitable membership fees. Charles Schwab is an online brokerage that doesn’t make any money from trading, instead passing their scale economics on to the customer in exchange for profitable net interest spreads on the customer’s cash balances.

In 2020, Charles Schwab stock sold off to near historic low valuations (unjustly) giving us the opportunity to finally purchase this great business. The value proposition to us was even greater given that Charles Schwab had also just completed the very accretive acquisitions of TD Ameritrade and the USAA asset management arm, providing us with a huge margin of safety on our purchase price.

FIRST AMERICAN FINANCIAL CORPORATION

First American Financial Corporation (FAF) is one of the two dominant players (along with Fidelity National Financial) in the title insurance industry. They are the sort of very profitable, dependable, defensible company, providing a keystone service, which tends to be overlooked by many investors seeking something a bit more exciting.

Under American law, the title of a house is not recorded in a centralized government database. Instead, title records are held in a wide variety of local databases, often consisting of unstandardized records with things like property boundary lines found in hand-drawn maps. This makes these types of records particularly difficult to standardize in order to speed up the title underwriting process.

This is where the title insurers come into play. Over their hundred-plus years of existence, they have been able to build up multiple centuries worth of data in each of their specific geographies in databases called “Title Plants”. The complexity of these title plants, as well as the need to forge relationships with key market participants (real estate agents, bankers, lawyers, etc.), has led to the consolidation of the industry into a small group of large players, with very little price competition.

Since title insurance is a policy to protect against the past, a title insurer’s ability to avoid losses is dependent on how well they conduct due diligence. For example, only about 4% of FAF’s premiums go to paying out claims (and these are usually fraud related). 85% or so of the premium (less over time with efficiency gains) goes toward operating expenses. For comparison, a normal property and casualty insurance company has an 80% loss ratio and 20% expense ratio. As such, we believe the market is mischaracterizing FAF’s economics when they lump them in together with other insurers.

We believe that FAF’s stock price was punished unfairly in 2020 considering the underlying strength of their end markets- this was likely due to a Wells notice (and subsequent lawsuit) they received from regulators regarding a data breach in 2019. Management believes this inquiry will be non-material, and our analysis suggests the same.

Going forward, what we get here is a very well defended business with strong underlying returns, and even if the macro picture does not improve, we can likely still expect low double-digit returns going forward. If the cycle does improve and efficiencies continue to be extracted from the business, there is room for significant upside.

UNITED PARCEL SERVICE

UPS is a great example of a company that has for many years been undervalued and underappreciated in the market – something we’ve been talking about for a number of years, and which arguably was finally recognized during 2020. UPS is the largest package delivery company in the world, delivering an average of 20 million packages per day across 220 countries. In terms of global networks, it is hard to beat. The opportunity presented to us in UPS stock is that the market is overstating the competitive risks UPS faces. In order to understand why we believe that to be the case, one must look ‘under the hood’ of the main players in this market- UPS, FedEx, and now recently – Amazon.

Both FedEx and Amazon have grown their delivery businesses very quickly, but they crucially have done so at much lower returns – i.e. they are much less efficient (this is partly estimation regarding Amazon, but the reasoning will become clear in a moment). Why does UPS consistently earn 20%+ returns on capital, whilst FedEx can’t even get to 10%? The answer is that UPS is a totally integrated model- they own everything: ground, air, express, trucks, planes, etc. Both FedEx and Amazon are franchised- meaning they have agreements with franchisees, and as such are restricted in how they can optimize their own routes and services. UPS have total freedom to optimize and structure their operations in whatever way is most efficient- that is a structural advantage that cannot be replicated. And is one that is misunderstood and overlooked by the market. It arguably took the huge global lockdowns during 2020, and the resulting ballooning of ecommerce and delivery, to highlight the real power and value of the UPS network. COVID 19 arguably advanced the already fast-growing ecommerce market by 5 years or more- exposing a lack of capacity in the global logistics network and highlighting the incredible value that exists within UPS.

Despite the considerable short-term appreciation in stock price, UPS remains very good value today. While the market has finally woken up to the value and the moat that exists within and around UPS, there has also been a significant industry shift- that of pricing power. For years, the logistics providers have only been able to put through relatively minor price increases- but with the capacity constraints exposed during 2020, they have been able to do much more. And given the fact that we will not be seeing substantially more capacity in the near future, we have likely now entered a new phase for the industry, one where pricing power is likely to be a feature for a number of years. This provides a significant cash earnings boost to UPS and it remains an incredibly well-defended cash producing asset for us.

CROWN CASTLE INTERNATIONAL CORP

Like American Tower, Crown Castle is an owner of cell phone towers. Whilst CCI benefits from the same incredible economics and cash flow generation from its legacy towers business that AMT does, CCI is choosing to reinvest its considerable cash flow into a different end market.

Within the US, it is incredibly difficult to build more large cell towers- obtaining zoning for a 300ft mast that may or may not cause health concerns is incredibly difficult. But that presents a problem- the towers are the bottleneck in our increasing usage of mobile data- there just simply aren’t enough of them to carry all the data people are now consuming on their mobile phones. This problem is only worsening as we move to 5G, the Internet of Things, and connected vehicles.

One answer is small cells- effectively mini-towers that are placed on lamp posts, traffic lights, etc. in dense urban areas. These small cells are linked by fiber optic cable, placed up and down streets and on buildings, to offload capacity from overloaded macro towers nearby. They are a very fast-growing market, but one which is dependent on owning the fiber backbone. CCI has spent $14bn buying and installing fiber miles over the last five years, now making them one of the largest owners of fiber optic cable in the 25 largest metro areas in the United States. This has been a very heavy upfront investment- one the market as a whole tends not to like as the returns are currently low. But the market isn’t looking far enough into the future- this fiber backbone gives CCI many years of capacity on which to roll out small cells. They can gradually densify their networks, such that cash returns in the future should be vast compared to those today. Crown is the leader in this space and is likely to remain so given their huge fiber portfolio. We see management as having made the hard decisions to invest now for returns tomorrow. We intend to partner with them to enjoy those future returns. In the meantime, we are supported by substantial cash flow from the existing tower portfolio and, as investors, enjoy a 3.5% dividend yield.

AMERICAN TOWER CORPORATION

American Tower is a wonderful example of a company that lies squarely in the middle of a huge, multi-decade trend. This trend is the exponential growth of mobile data consumption driven by ever-increasing smartphone penetration, faster available mobile internet speeds, huge growth in content (particularly video such as Netflix, Disney+, etc.) being consumed on mobile devices, as well as the huge growth in the number of internet-enabled devices.

American Tower being one of the largest owners of cell towers in the US (along with Crown Castle, which we also own, for different reasons). These are incredibly valuable assets, as they are arguably the bottleneck when it comes to us all consuming more and more mobile data. American Tower simply owns the tower and rents space to the carrier companies (AT&T, Verizon, etc.) on very long-term contracts to fix their equipment on – which results in a low fixed cost, stable, hugely cash generative business. a very efficient business model. These towers typically have 10-20-year inflation-linked contracts with the carriers. It is very hard to build any new towers as zoning is so difficult to achieve, so there is little competition. The cash flow predictability is exceptional, and American Tower is taking this cash flow and reinvesting it into new towers (and portfolios of existing towers) in faster-growing and much earlier stage markets like Brazil and India, providing a tremendous growth runway.

In 2020, American Tower underperformed the market as a whole – not for fundamental reasons, but for what appears to us to be a rotation away REIT companies which on average do poorly in a rising rate environment. The market’s grouping of American Tower in this sell-off bucket is a mistake, and we will gladly increase our position at the market’s cost.

In the end, this is a growing business very unlikely to be disrupted – no political party, individual company or country can do much to stop it. Valuation permitting, we could conceivably own American Tower for decades to come.

ALPHABET, INC.

Google’s core business is search advertising, where AdWords has proven to be one of the best businesses of all time – when you hear companies talk about customer acquisition costs, what they are really talking about is paying their toll to Google. Google’s position as the dominant tollbooth between customers and businesses wanting to reach those customers is extremely well protected due to the network effects involved in search engines, and the data feedback loop that makes those search engines better over time.

That incredible search business has allowed Google to aggressively expand into many other industries – email, hardware, cloud computing, mapping, autonomous driving, etc. The acquisitions of YouTube, DoubleClick, and Android have proven very lucrative for shareholders, and as such we have grown comfortable with the way management allocates our capital. However, if at any time management chooses to dial back those investments, the amount of cash that could be returned to shareholders would be far in excess of what today’s financial statements would suggest.

In 2020, Google’s stock performed well despite numerous regulatory lawsuits filed against them (often the case). We believe that these regulatory worries are unwarranted. For one, the service Google provides is extremely valuable to end-users and is also free. Two, if Google was broken up, it would probably increase Google’s total market value – an unintuitive outcome that is due to something known as the conglomerate discount (for example, YouTube’s growth might be masked by other slower growth segments, AdWords margins might be masked by other lower-margin segments, etc.).

Going forward, Google’s growth will arguably be a function of the time people spend online – a secular trend that we believe is in our favor.

Conclusion

As always, please feel free to reach out to us with any questions you may have. As we said at the beginning, we greatly appreciate the continued trust and confidence that you have placed in us.

We extend our best wishes to you and your families for a healthy and prosperous 2021.

Best regards,

Guy Davis, Pas Sadhkuhan, Shaumo (Neil) Sadhukhan, David Shahrestani

Disclosures: This website is for informational purposes only and does not constitute an offer to provide advisory or other services by Globescan in any jurisdiction in which such offer would be unlawful under the securities laws of such jurisdiction. The information contained on this website should not be construed as financial or investment advice on any subject matter and statements contained herein are the opinions of Globescan and are not to be construed as guarantees, warranties or predictions of future events, portfolio allocations, portfolio results, investment returns, or other outcomes. Viewers of this website should not assume that all recommendations will be profitable, or that future investment and/or portfolio performance will be profitable or favorable. Globescan expressly disclaims all liability in respect to actions taken based on any or all of the information on this website.

There are links to third-party websites on the internet contained in this website. We provide these links because we believe these websites contain information that might be useful, interesting and or helpful to your professional activities. Globescan has no affiliation or agreement with any linked website. The fact that we provide links to these websites does not mean that we endorse the owner or operator of the respective website or any products or services offered through these sites. We cannot and do not review or endorse or approve the information in these websites, nor does Globescan warrant that a linked site will be free of computer viruses or other harmful code that can impact your computer or other web-access device. The linked sites are not under the control of Globescan, and we are not responsible for the contents of any linked site or any link contained in a linked site. By using this web site to search for or link to another site, you agree and understand that such use is at your own risk.